ANZ, CBA, NAB and Westpac share their thoughts

The complexities and challenges of 2020 have been very different to those of recent years. They were not born out of commissions, changes in legislation or economic impacts. The industry – like all industries – has had to navigate the environment without really knowing what lies ahead. As one of the big four began by saying, there has been no blueprint for this year.

When borrowers started losing their jobs, or having their salaries reduced, brokers kicked into action to help find a solution. At the same time, many borrowers saw the changes and incentives from the government as their opportunity to get into the housing market. In this year’s Major Banks Panel, the heads of third party at the big four had the opportunity to explain how they were supporting brokers as they adapted in the face of these changes.

Of course the pandemic also meant that MPA’s annual livestream interview with the major banks had to be done virtually this year; three of the four participants live in Victoria so were definitely not able to join an in-person event.

Rather than holding the interview behind closed doors – or screens – we felt it was important to continue the tradition of the live interview with the big four, allowing brokers unedited access to what the major banks had to say. And while there were the usual challenges that come with virtual conversations, such as connection issues and being unable to read body language, everyone is more or less used to this way of conducting business now, so the panel discussion ran fairly smoothly.

There were questions prepared beforehand, but we also received more than 200 questions from brokers. The strong engagement was not surprising after the last few months. Most of the questions received were on bank turnaround times and SLAs, which became the main focal point of the conversation.

The topic that attracted the second-highest number of questions was channel conflict. A number of brokers said they were facing slower turnaround times than if the customer went directly to the bank, as well as different policies.

The four major banks tackled these topics and more during the hour-long conversation. Read the full report on the following pages, and if there are any further questions you have, the banks are encouraging brokers to reach out to their BDMs.

Thank you to the major banks for taking the time to join in on the day, and to all the brokers who watched and sent in questions.

Q: We’ve all faced a difficult year, and brokers have worked hard to navigate the complex environment. What are you doing to reassure brokers that you are working in their best interests?

At the start of 2020, the broking industry was full of positivity. Almost a year on from the royal commission’s final report, brokers were going into a year in which things were going to be clearer and more certain, or so they thought.

“There’s a lot coming from every lender out there, so we’re just trying to make sure we’re clear and simple in our communications” Adam Croucher, Commonwealth Bank

Instead, the first year of the new decade turned into the least clear or certain period many had ever experienced. As life changed for people across Australia, brokers switched into gear. Keeping up with the stream of updates from banks and the government, they helped borrowers refinance, organised repayment pauses, supported small businesses needing finance, and dealt with first home buyers trying to get onto the property ladder.

The major banks began the livestream panel by thanking brokers for their hard work over the last several months.

The major banks began the livestream panel by thanking brokers for their hard work over the last several months.

Warren Shaw, head of broker distribution at Westpac, said brokers were uniquely placed to play the role they have this year. As thousands of small businesses across Australia struggled with consumer caution and lockdowns, brokers were among them, understanding their issues better than any large organisation, he said.

“Westpac sees it as a partnership in terms of helping customers through the times that we’ve been through in the last eight months, and there are a number of things that we’re doing to support customers clearly, and brokers,” Shaw said. “But first and foremost, it’s about working with mortgage holders to make sure we don’t put customers in a position that they can’t get out of.”

Shaw mentioned actions like repayment pauses and individual assessment of needs, which many banks introduced earlier in the year. He said Westpac joined other lenders in acting quickly at the outset to reassure brokers that trail would not be affected, and provided both technology and policies to help brokers’ customers – but he admits it was not all smooth sailing.

“Technology normally outpaces policy, but in the last few months we’ve had policy changes to adapt to dealing with people remotely, where technology hasn’t kept up,” Shaw explained. “I think as we get those changes in they’ll get better, less clunky, but it was all about acting with speed, and that was the key thing to give people confi dence in the system.”

ANZ’s general manager retail bank, Simone Tilley, added that it had been a huge year for everyone, praising what had been achieved as “remarkable”. Priding itself on its partnership with brokers, ANZ has delivered key changes to the market beyond just the pandemic.

Tilley gave examples of the bank’s qualitative file reviews and net-of-offset commission changes. Leaders at ANZ are also active in the Combined Industry Forum, with Tilley herself becoming co-chair earlier this year.

“We also saw record volumes, the highest in ANZ’s history, and those volumes were unquestionably driven by the partnership we have with Australian brokers” Simone Tilley, ANZ

She also called out the bank’s investment in its BDMs, its operating model and education programs, as well as the services it has offered due to the pandemic, with support including a free confidential wellbeing service for brokers and staff.

“We did this just to ensure that we’re doing everything possible to support the industry during these unprecedented times,” Tilley said, but she acknowledged there had been some challenges.

“We know this year we’ve had SLA deterioration, but one thing I do want to reiterate is that every single week we send a note out to aggregators sharing our SLAs across refinances and purchases just so you’re able to communicate and manage the customer’s expectations along the way,” she explained.

“I’m confident that, SLAs aside, when brokers think of ANZ more broadly, they know we act in the best interests of brokers, and I think we’ve evidenced this over an extended period of time.”

On top of similar wellness events and keeping brokers on top of their borrowers’ circumstances in terms of things like deferred repayments, NAB has put its focus on speeding up innovation to cater for the inability to meet face-to-face.

Making sure that brokers could not only continue to write business and speak to customers but also do so in a way that complied with regulations, the bank introduced facilities like DocuSign. Within two weeks of the first lockdowns NAB staff were up and running, supporting brokers in virtual sessions.

“It was really important to us that we provided excellent service to brokers, who once again as small business operators or single operators would be by themselves, so we very quickly adapted,” said Steve Kane, NAB’s general manager, broker distribution.

“It’s imperative that if you’re going to be in this market you recognise the value that brokers contribute. Where there were massive changes that were happening because of COVID-19, it was our responsibility to do as much as we possibly could on a technology front, a relationship front and a support front.”

Echoing the sentiment of the previous three speakers, Commonwealth Bank’s general manager, third party banking, Adam Croucher, said what had been achieved over the past year was phenomenal.

He said one of the areas the major bank had been focusing on was making sure it had the data and analytics to get brokers through this challenging period; it also added more than 600 extra staff to its financial assistance lines to support both brokers and customers.

Croucher said that while it would be great to have all the answers, lenders had done an excellent job of being agile and feeding infor-mation back to the aggregator groups.

“Beyond the economic impacts, brokers have had to stay up to date with regular policy changes,” Croucher said.

“One area we’ve been really focused on is making sure they have direct access to credit managers so that brokers can stay up to date by having regular conversations with our credit assessors.

“First and foremost, it’s about working with mortgage holders to make sure we don’t put customers in a position that they can’t get out of ” Warren Shaw, Westpac

“I think we’ll continue to see a number of policy changes over the next few months, and a key differentiator for us is making sure that our dedicated support, our relationship managers, our phone lines and our CommBroker email blasts are up to date and relevant. But we also understand that there’s a lot coming from every lender out there, so we’re just trying to make sure we’re clear and simple in our communications.”

Q: What insights can you share from the last six months? What kinds of borrowers have come through to you?

Q: What insights can you share from the last six months? What kinds of borrowers have come through to you?

The four major banks have all seen similar trends over the past year: while some borrowers needed help with their repayments, new business continued to come in to the banks.

Looking back at 2020, Croucher said he had seen significant shifts. For instance, for the first time internal and external refinancing accounted for more than half of all mortgage lending at CBA.

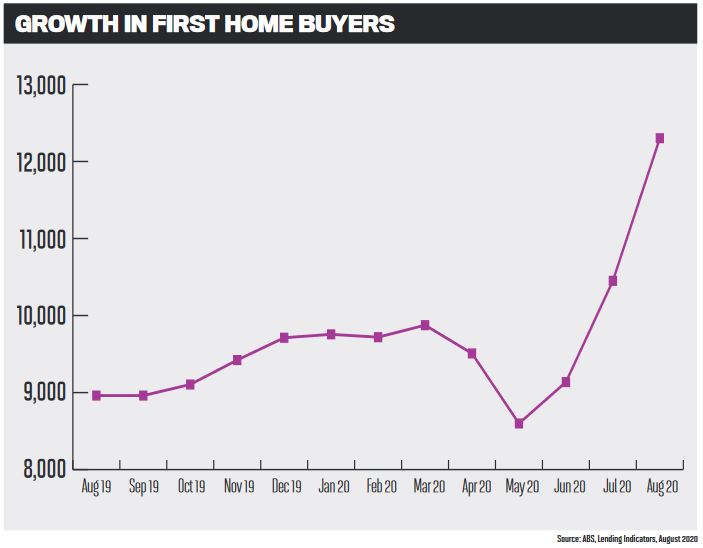

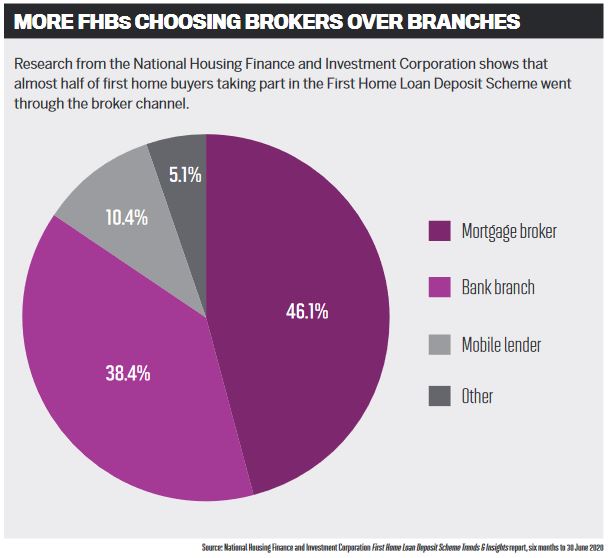

First home buyers have also been a strong segment this year as new borrowers were supported by the First Home Loan Deposit Scheme. As one of two major banks participating in this scheme, CBA has helped around 3,000 first home buyers purchase new properties.

“We’re also seeing a large shift towards fixed rates, from nearly 10% of new business flows prior to March to nearly 40% of volume in June, driven by historic low fixed rates,” Croucher said. “So there are certainly some trends that we’re seeing, and we’re expecting to see those trends continue in the short to medium term as we enter a sustained low-rate environment.”

ANZ has seen the same in terms of the rise in refinancing and fixed rate loans. Tilley also pointed out the work the bank had done with brokers and customers, particularly in the earlier stages of the pandemic. It sped up innovation, worked with its branches to reduce human contact, and assisted customers with requests for loan repayment deferrals.

Alongside the increase in borrowers wanting to refi nance or fix their mortgage rates, Tilley said ANZ had run a campaign that saw huge success.

“That really took off, but now I have to say we are really back to far more normalised, sustainable levels,” she said.

“We also saw record volumes, the highest in ANZ’s history, and those volumes were unquestionably driven by the partnership we have with Australian brokers.”

NAB also experienced high levels of refinancing thanks to strong incentives, and Kane said this had created a problem for service. But with NAB’s financial year ending in September, he said it had probably been the strongest year for the broker business since he joined the bank.

Shedding further insight into first home buyers, Kane said around 45% of this market were borrowing for new builds.

Furthermore, he added, “We know that around 65% of all applications approved by NAB came through the broker channel, so the broker channel supported customers in that area strongly, and that’s a very good thing because that’s enabled first home buyers to get into the marketplace.”

Expecting refinancing to remain strong into 2021, Shaw noted that purchaser activity had also been high at Westpac, but investor activity had dampened. He added that this had created the opportunity for first home buyers to get into the market, which was “a great thing”.

Looking ahead, Shaw said people were going to begin considering what the next 12 to 18 months were going to look like, and this could be good news for brokers.

Looking ahead, Shaw said people were going to begin considering what the next 12 to 18 months were going to look like, and this could be good news for brokers.

“We’re starting to see some customers think about lifestyle choices: whether the home they live in is going to be suitable for long-term working arrangements from home in particular,” he said.

“If you look at the search engines you see a 30–40% increase around searches or things like studies and gardens and those aspects, so I think the broking community should feel quite buoyed by the fact that there’ll be strong underlying purchase activity through 2021.”

Q: A number of brokers have sent in questions around channel conflict, saying that customers get better turnaround times and credit policies by going directly to a bank branch. Are you doing anything about that?

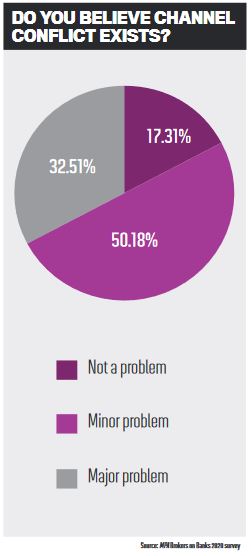

In this year’s Brokers on Banks survey, eight in 10 brokers said channel conflict was a problem. The issue has clearly not diminished in the eyes of brokers, as it was the topic that received the second-highest number of questions in the lead-up to the panel discussion.

“COVID hasn’t been easy for us [but] I’m very proud that we’re making sure we’re looking at the best interest of the customer” Adam Croucher, Commonwealth Bank

Brokers asked why loans were processed faster through a bank branch than through a broker and why branches were able to offer better deals than brokers. Others asked how the banking culture could change to enable banks and brokers to work together.

The first to respond, Kane said there was no difference between credit policies for the first party and third party channels, and where conflict did arise NAB followed the direction of the customer. If there were duplicate applications, the bank would speak to the broker and review any discrepancies in decisions. He said incidents like these did not happen often, but they were taken seriously when they did.

“First and foremost, it’s about working with mortgage holders to make sure we don’t put customers in a position that they can’t get out of ” Warren Shaw, Westpac

“For NAB, the broker channel provides signficant introduction of brand-new customers, new business and opportunity,” Kane said.

“We don’t prefer any channel. If the [customer] chooses to use a broker, or if they choose to come via the proprietary channel, that’s the customer’s choice, and we will honour their choice.”

“We don’t prefer any channel. If the [customer] chooses to use a broker, or if they choose to come via the proprietary channel, that’s the customer’s choice, and we will honour their choice.”

Looking at how brokers and the retail channel could work better together, NAB has been trialling a service that enables retail bank staff to work with broker-introduced customers and the broker in order to ensure a smoother application and transaction process. It will be rolling that out soon, allowing brokers and customers easier access to the bank when they need it.

NAB has also made a number of changes, driven by the need for a one-way process for home lending regardless of what channel it comes through.

“That process has begun already, and brokers will see the results of that coming through in mid to late FY2021, when there will be absolutely no difference whatsoever in the processing of home loans regardless of how that customer enters the bank,” Kane said.

Agreeing, Croucher said it was incumbent on the bank to make sure “the customer holds the key”. CBA has worked over the past two years to understand how duplicate applications happen, and while this means that they very rarely occur now, when they do, the bank continues to try to learn what it can do differently and consults with both the customer and the broker.

While credit policies do not differ between the first and third party channels, Croucher said turnaround times were a little more difficult.

“We have proprietary being able to verify under the bank licence, so there’s always going to be some difference there,” he said.

“I can’t apologise for that. In the third party channel things have to be verified the way that they are, but we will try to make that process as simple as we can so that there is no differentiation in the turnaround times.

“COVID hasn’t been easy for us, as we’ve all explained, with the complexity faced by the industry, but I can certainly say I’m very proud that we’re making sure we’re looking at the best interest of the customer and learning from any examples of where there is poor behaviour.”

While Shaw said there would always be friction at the edges of any multi-channel business, he added that it was something the bank was continually getting better at. Although he had not seen an increase in channel conflict, where it did happen he said the bank worked to satisfy itself as to which channel the customer wanted to deal with.

In terms of the differences arising between turnaround times and credit policies, Shaw said Westpac had invested millions of dollars in a one-banking platform that would be coming to the broker channel in 2021 and should provide a more consistent experience.

He added that trying to eliminate conflict often in fact created longer turnaround times.

“If my first party colleagues want to put a campaign on to support their sales eff orts, I’ve got two choices: either support that and manage the elongated wait times, or I create conflict by not allowing those offers to be put into the third party channel, and that creates a whole other set of issues,” he explained.

“I’m confident that, SLAs aside, when brokers think of ANZ more broadly, they know we act in the best interests of brokers” Simone Tilley, ANZ

“I’m sure there is no one watching who would rather not have the ability to give an off er to a customer, whether it be a rebate or a very good fixed rate, for example. They’d much rather be able to manage the customer’s expectation and deal with those customers with that offer.”

Conducting a “channel agnostic” strategy, Tilley said, ANZ recognises the importance of brokers and gives no preferential treatment to one channel over the other. But she added that there had been SLA differentiation and she was keen to explain why.

“We have had a long-established process of auto-decisioning in our network business due to the fact that they can complete document verification, and we are now adopting an automation program across broker and mobile channels so that similar levels of automation can be adopted across all channels,” Tilley said.

“Given the large volume that has come through the broker channel, which at this point is 100% manually assessed, there have been unintended SLA differences which we are working hard to address.”

Q: What are you doing to ensure that brokers can provide answers to their customers in a fast time frame?

Q: What are you doing to ensure that brokers can provide answers to their customers in a fast time frame?

All four of the major banks admitted that there was more work to do after the broker channel saw lengthier turnaround times this year.

Volumes at ANZ had definitely had an impact on SLAs, Tilley said, but even leading up to the pandemic the major bank was working on streamlining the home loan processes by investing in its people and technology, which meant that it could act fast when COVID-19 did have its effect.

“We implemented a taskforce dedicated to improving our work in progress, which has assisted us in reducing assessment times and also improving capacity, because we recognise we need to do more,” she said.

This goes along with the innovations ANZ has introduced in recent months, such as digital verification, Illion’s Access Seeker and automation processes.

“If the [customer] chooses to use a broker, or if they choose to come via the proprietary channel, that’s the customer’s choice, and we will honour their choice” Steve Kane, NAB

“The measures we’ve put in place over the last few months will unquestionably improve the robustness of our processes, and we intend to continue that work as we go,” Tilley added.

Croucher said CBA had maintained strong SLAs as it went into the “perfect storm” that was the First Home Loan Deposit Scheme, the Homebuilder scheme and the pandemic. In the nine weeks prior to the panel, he said the bank had recorded around 7,000 hours of overtime.

“There’s those impacts that we all felt as a result of the extended flows at the start of COVID and the consistency across the period that we are in at the moment, so I think for us to maintain five days has been really key,” he said.

“It’s very expensive, but the commitment to make sure that we keep that agreement to a controllable level has been exceptionally important to us.”

Westpac has also spent the last seven to eight months putting new processes in place to deal with things either from a credit perspective or make it easier to help customers and assist them in meeting requirements. It has also moved a number of its resources away from other areas in the bank in order to assist customers in hardship.

Westpac has also spent the last seven to eight months putting new processes in place to deal with things either from a credit perspective or make it easier to help customers and assist them in meeting requirements. It has also moved a number of its resources away from other areas in the bank in order to assist customers in hardship.

As part of its continued efforts, the major bank is also bringing jobs back onshore. While its offshore call centre arrangements had worked well in the past and allowed Westpac to increase capacity, Shaw explained that large-scale shutdowns due to the pandemic had caused a problem.

“Westpac announced a while ago that we would bring back onshore call centre activity and mortgage processing activity in the next 12 months,” he explained.

“The mortgage broker side of things will be impacted first, so we are recruiting now to stand up those resources onshore, and that just takes out of the equation any instance of us not being able to manage the disaster recovery situation better and have it in our control. It’s important for the economy as well; clearly, 1,000 jobs are well needed here, and we’re happy to support it in that way.”

To help with turnaround times at NAB, Kane said the biggest focus was on technology to make sure processes were smooth and simple so the possibility of mistakes slowing down transactions was reduced. NAB is working with NextGen.Net on several areas, in order to help give brokers a much clearer and automated picture of what is missing.

“We have a strong focus on delivery of service,” he said. “There is absolute understanding that the broker’s reputation and the veracity of their ongoing referral basis is always underpinned by the service of the lender they’ve recommended. So, if we don’t provide a good service it impacts on the broker’s reputation, and we’re very focused on that.”