Variable rate transition already peaked, says CEO

ANZ says the bulk of its fixed rate customers have already rolled on to higher variable interest rates during a bumper second half.

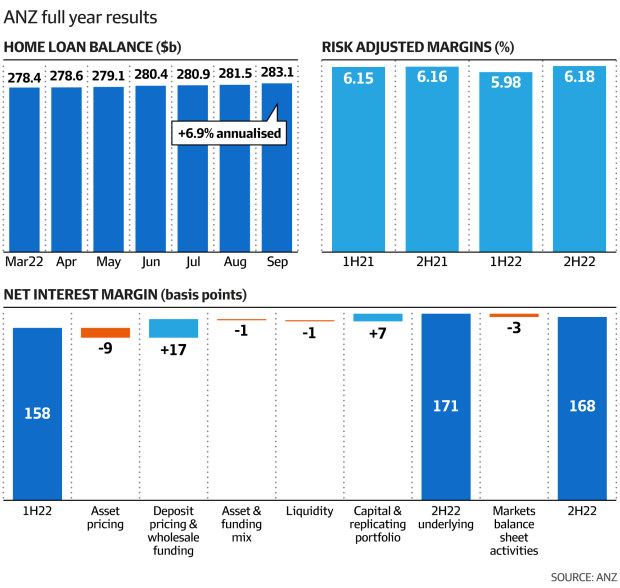

The big four bank reported a 5% lift in its full-year cash profit and a 0.13 percentage point increase in its net interest margin.

ANZ handed down a $6.5bn profit on October 27, with one of the fastest interest rate increasing cycles in history helping to deliver half of its revenue growth, the Australian Financial Review reported.

This month the RBA warned of a looming “fixed rate” cliff as customers roll from ultra-low onto sharply higher variable rates. But ANZ CEO Shayne Elliott (pictured above) told the AFR that the bank’s transition had already peaked.

Read next: ANZ steps up Suncorp merger plans

“The largest number of rollovers was in the last half of 2022,” Elliott said. “We’ve had the worst behind us.”

Hinting at what lies ahead for other banks, where the bulk of fixed rates roll off in 2023, Elliott said about 80% of fixed rate customers had stayed with ANZ.

Its ANZ+ retail banking business under Maile Carnegie delivered strong growth, tied to its attractive 3.25% interest rate on transaction balances up to $250,000.

The AFR reported that the much higher deposit rate competed with Macquarie’s rate for savers and had spurred huge inflows. ANZ+ had quickly gathered $1.2bn in deposits. Elliott said the growth trend should continue.

“I think it is going to be a point of differentiation in the coming year,” he said.

While market share had gone backwards in the first half, ANZ’s home loans business enjoyed 6% cent growth in the second half.

Elliott said the bank’s performance was now in line with the rest of the market.

“We restored momentum in Australian home loans with application approval times back in line with industry peers,” he told the AFR.

“We continued the re-platforming of Australia Retail onto ANZ Plus, which is our new digital bank, with deposits already exceeding $1.2 billion and growing at a rate faster than any new digital bank in Australia.”

Overall net interest margin (NIM) expanded to an average 1.71 percentage points in the September half from 1.58 percentage points in the March half, and a running rate of 1.8 percentage points in the month of September. The RBA lifted the cash rate from 0.1% to 2.6% over the same period.

Jarden analyst Carlos Cacho said ANZ’s second-half margins were slightly better than expected given the benefits of deposit pricing added 17 basis points. The banks charge more for their loans than they pay their depositors, helping to boost their returns.

Read next: ANZ expands executive roles

Cacho told the AFR that the better-than-expected exit NIM – which captures where ANZ ended the full year period in September – spelt “material upgrades” to consensus earnings for the banks.

“More importantly, the outlook on margins was better, with the September exit margin of 1.80% ahead of consensus first half margins of 1.73%,” he said.

Citi analyst Brendan Sproules warned that inflation and increasing investment in growth would push ANZ’s costs higher.

“We expect that management may be accelerating investment given the stronger revenue environment, with a higher share shifted towards growth investment,” Sproules said.

“Offsetting NIM upside is higher costs, which have been guided to increase by 5% in the current financial year, as cost inflation rears its head. Despite the surprising higher cost quantum, on balance, we think that consensus core earnings gets revised higher post this result.”

ANZ will pay a final dividend of 74¢ a share on December 15, up 2¢.

It released provisions of $232m during the period but continues to hold $3.853bn. Elliott defended suggestions that the bank is too positive on the outlook, saying a bigger deterioration was “extraordinarily unlikely”, which shows the strength of the whole banking system.