Business failure rate sees 8.8% increase across all industries

There was a significant decline in the value of invoices held by Australian businesses, driven by waning consumer demand and reduced inventory levels, CreditorWatch’s latest Business Risk Index has revealed.

The average value of invoices held by businesses fell by 49.9% year-on-year to June 2024, reflecting a sharp drop in order values as companies cut back inventory due to higher prices and declining demand.

Compounding the issue is a rise in invoice payment defaults, which have been increasing since mid-2021. This trend suggests that businesses are struggling to pay their suppliers despite reduced order values.

CreditorWatch also reported an 8.8% increase in the business failure rate across all industries over the past year. The outlook for the hospitality industry has deteriorated, with the failure rate expected to rise from 7.5% to 9.1%, significantly higher than the forecasts for the arts and recreation services (5.7%) and transport, postal and warehousing sectors (5.5%). The average forecast for all industries stands at 5.1%.

The high forecast failure rate in hospitality is largely due to its dependence on discretionary spending, which has declined as consumers face higher mortgage payments, rents, and utility bills.

Business payment defaults dipped from May to June but have been trending upwards since mid-2021, exceeding pre-COVID levels. Rising costs and declining demand are squeezing businesses, making it harder to pay suppliers. CreditorWatch has identified a strong correlation between B2B payment defaults and the likelihood of business failure in the following months.

“The combination of declining order values and increasing payment defaults is a major concern as it indicates more businesses are experiencing both cost and demand pressures,” said Patrick Coghlan (pictured above left), chief executive of CreditorWatch. “With another rate increase becoming increasingly likely, we expect both metrics to deteriorate even further.”

“It is small businesses that are hurting the most as they are more vulnerable to adverse economic conditions than larger businesses. They operate on tighter margins and are less able to take measures to cut costs.”

According to Anneke Thompson (pictured above right), chief economist at CreditorWatch, we are now well and truly in the toughest phase of the monetary policy cycle.

“The high cost of debt is compounding the problems wrought by inflation, that is still too high in some areas,” she said. “Monetary policy decisions usually lag what is happening in the broader economy, as data takes time to filter through to the RBA, and the RBA also wants to see a few months’ worth of data to be more certain that their decisions taken at board meetings are the correct ones.

“While this approach is sound theoretically, in practice, it means businesses have to endure high interest rates long after consumer demand has plummeted, and discretionary spending has significantly weakened.”

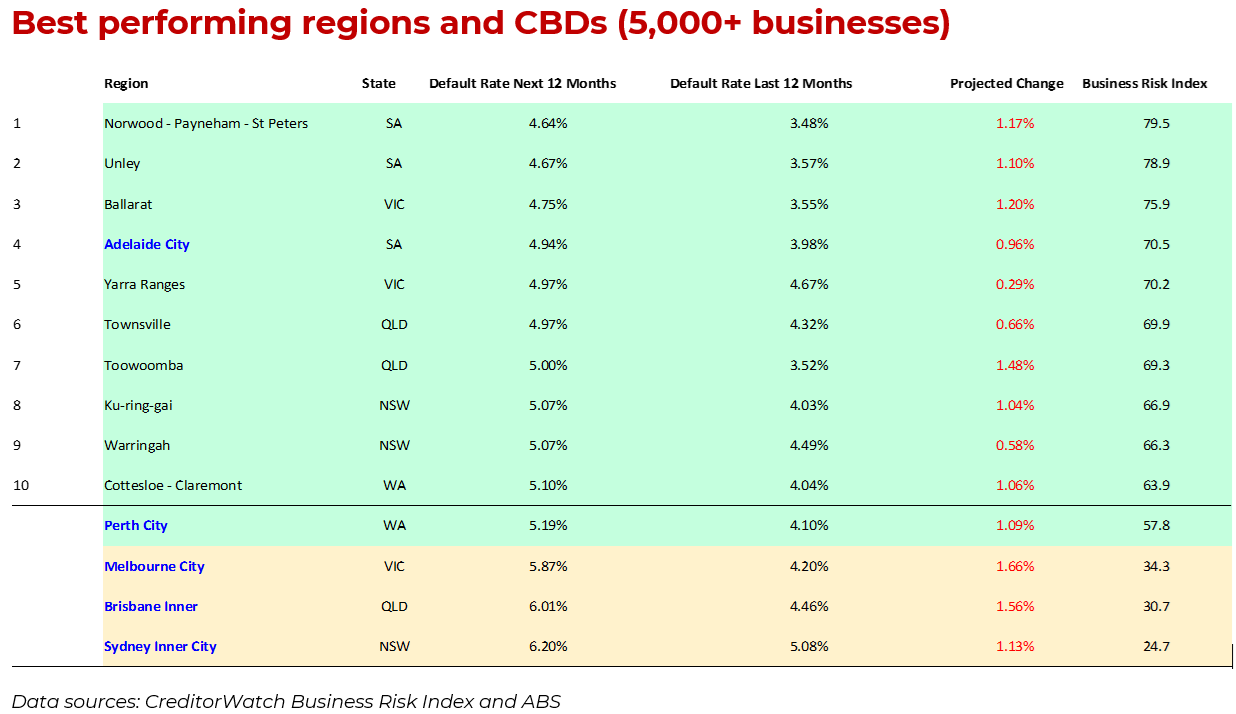

CreditorWatch also found that the best-performing regions continue to be those with a higher proportion of older businesses and residents, who typically have lower rates of personal insolvency. Adelaide City remains the safest CBD in terms of insolvency risk, benefiting from relatively low rents and a significant number of workers and international students.

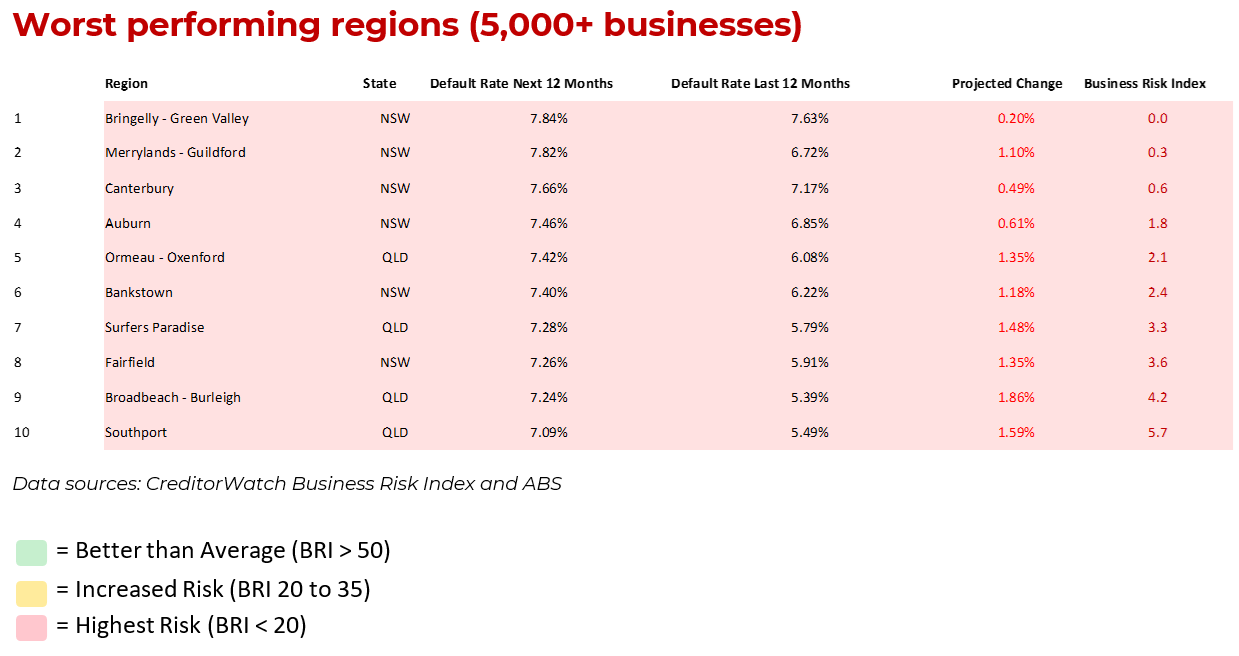

The hardest-hit areas are those with younger populations and businesses in the hospitality sector. This trend is expected to continue into 2025, with significant business failures and a likely rise in unemployment.

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.