Five reasons why professional services firms offer brokers solid possibilities

Professional services businesses are found in almost every city, town and suburb. What’s more, their resilience through economic upheavals and their low credit risk are drawing strong interest from brokers.

The position of professional services businesses has strengthened over the past 10 years, with economic storms and uncertainty driving demand for their expert advice.

Professional services span accountancy, legal, real estate, medical and health, financial planning and insurance broking businesses. Their intrinsic resilience comes from their high profit margins, high revenue per employee and broad client bases (reducing client concentration risk).

Less dependent on capital infrastructure (such as plant and equipment) and with little reliance on imports and exports, these firms are better able to control their operating environment than other businesses. This means professional services firms can rapidly adapt to disruptions – as they did in 2020 when government requirements suddenly forced their employees to work from home.

That makes them an attractive proposition for lenders and, consequently, a good opportunity for brokers.

How professional services firms offer opportunities for brokers

It’s not surprising that brokers are taking a closer look at finance opportunities among professional services firms. Here’s what’s attracting them:

1. Numerous, geographically distributed and growing

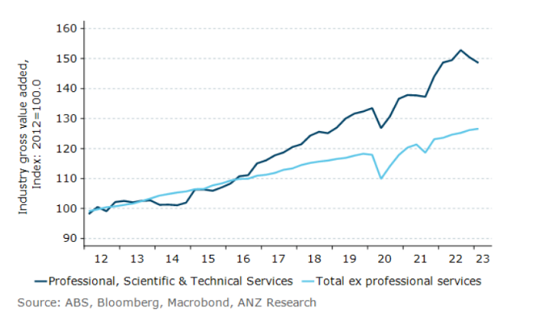

Professional services firms are a major part of the Australian economy, generating $272.6 billion in revenue in 2022, according to IBISWorld data. Over the decade to 2023, their collective output grew faster than for other industries, as shown in figure 1. Growth has accelerated since 2021 – though activity eased through 2022 and early 2023.

Output from professional services outpaces other industries

2. Lower credit risk

Professionals operate under significant scrutiny from their industry bodies and/or government legislation and this fosters higher standards of professional conduct. Fran Babic, Head of Professional Services Commercial Bank at ANZ, says the credit risk for a professional services business is generally lower than for a standard business.

“That's because professional services businesses are generally a lower default risk compared to generalist businesses,” Babic says. “If we're talking about lawyers and accountants, for example, a bad loan could be a black mark, not only on their business, but also their personal reputation.”

3. Financial competence

Ruth Zhou (pictured below), Relationship Manager – Commercial Banking at ANZ, adds that because legal and accountancy business owners are financially literate, the work the broker needs to do for each transaction is generally lower.

“They've already done the work for you; they’ll already have a well-structured business,” says Zhou. “They know their financial data inside out and know if the business can afford to borrow more or not.”

“All the questions we have are likely already answered by the professional services borrower. They already know what security they can provide, rather than us try to work out how we can make the transaction work.”

Babic agrees: “Versus other business customers, professional services firms already know what they want. And they’ll get their own tax and legal advice.”

4. Event-driven financing

Typically, professional services businesses are event-driven borrowers.

“They borrow when they have a need, such as a merger or acquisition, purchasing a commercial property related to the business or succession planning,” says Babic. “Being event-driven, transactions are timely, and the purpose of funding is self-evident.”

5. Broad banking needs

In addition to lending, professional services customers have comprehensive transactional requirements.

According to Jarrod Fitzgerald, Senior Relationship Manager at ANZ, “it's a whole-of-wallet opportunity”.

“Real estate agents have rent roll and sales accounts that are governed by trust account requirements,” Fitzgerald says. “Solicitors and lawyers have the same kind of arrangements. Brokers can put together a whole package for these firms.”

Succession planning a priority for the sector

Themes that are playing out in the professional services sector include consolidation and the deployment of technology such as artificial intelligence and ChatGPT. But it’s the hunt for talent amid ongoing staff shortages that’s creating the most pain for business owners – and an opportunity for brokers.

As professional services firms depend on high-quality staff, they’re more likely to prioritise equity and succession planning as a staff retention tool.

“High attrition and demand for labour is certainly a big theme,” Babic says. “We're seeing a lot of staff being poached from other businesses – sign-on bonuses, higher salaries – and that's for junior staff right out of school. Professional businesses’ struggle to retain top talent.”

Fitzgerald adds: “We see people in their 20s buying in [to established businesses]. It’s very, very difficult in today's environment to attract and retain staff without offering something in return.”

Babic notes that, as a result, the typical make-up of a professional services firm is changing.

“Previously, there were two or three equity partners/owners and the rest were salaried staff. Now you’re seeing those junior staff coming in and owning only 2% or 5%, but at least there’s a stake in there – some sort of skin in the game,” says Babic. “They’re hungrier to stay in and drive the business.”

“I think that's what a lot of the older generation would like to see coming through before they formally hand off. So it's not uncommon to see smaller parcels of ownership instead of a complete 100% handover.”

There’s also a cohort of older professionals who are looking to retire now. “They want to get out while valuations are still pretty solid – divest and move on,” Fitzgerald explains.

Yet funds are needed to pay those high exit valuations. As Babic elaborates: “The issue here is that you have junior partners with high mortgage repayments, maybe young children. Interest rates are relatively high at the moment. They don’t have a spare $350,000 or $500,000 or $1 million lying around. Having a bank that understands the value of equity in a professional services firm – especially when the majority of the asset is goodwill and intangible – is really important.”

Professional services firms have higher borrowing capacity

When it comes to determining loan values, the lower credit risk for professional services firms means that these firms can generally borrow more.

For example, when lending to real estate businesses, it’s an advantage to consider the entire revenue stream.

“We look at the property management value, the rent roll books – how sustainable are they? What’s their quality as security assets? We also take into consideration the earnings from sales commissions,” says Babic.

“We’re looking at the overall revenue composition of a real estate agency and apply value to that. We tend to look at funding up to 70% of the loan valuation ratio (LVR) against rent rolls to reflect the value of those assets. We may go over that amount, as assessment is done on a case-by-case basis.

“Rent roll multiples have increased over the past 12 to 18 months. Historically multiples between 2.5 to 3 times revenue was the range you’d see. Today, we're seeing multiples at anywhere between 2.8 up to 4 in certain postcodes. They’re certainly a hot asset right now,” she says.

Wrapping up, Babic adds: “ANZ is focused on professional services lending in terms of how we're assessing risk and providing professional services businesses an alternative proposition rather than treating them the same as general business lending.

“It's a real game changer when you can assess a business, for example a real estate agency in its entirety, rather than just apply a broad-brush approach or a generic LVR.”

Learn more

To find out more about opportunities for brokers in Australia’s growing professional services sector and the specialist support ANZ provides brokers, contact your ANZ business banker or go to ANZ Professional Services.

And for a limited time, ANZ’s Lenders Mortgage Insurance premium costs are waived for eligible professional customers. For more information, click here.

This article is brought to you by ANZ

This is general information. ANZ is not giving advice or recommendations, and we haven’t taken into account your customers’ needs, financial circumstances or objectives. You and your clients should carefully consider which ANZ products are appropriate for them and should seek appropriate independent advice (which may include property, legal, financial, taxation and accounting advice) before making any decisions, investing, or acting on it. Terms and conditions, fees and charges, and credit approval and eligibility criteria apply to ANZ products.