Increasing prevalence is reducing borrowers' ability to cope if mortgage stress increase, experts warn

Over half of new home loans are being issued with 30-year terms, new Centrix data has shown.

There has been a steady rise in the proportion of home loans taken out at a 30-year term since 2017 as house prices rose – and this increasing prevalence was reducing borrowers’ ability to cope if mortgage stress increased, experts warned.

Some 57% of new mortgages taken out this year were issued at 30-year terms, with Auckland and Wellington seeing the highest proportion of borrowers taking out this longest-term option, at 66% and 55%, respectively, Stuff reported.

Thirty-year terms were also more common for first-home buyers, making up 83% of the group’s new mortgages this year – up from 74% over the past three years.

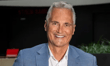

Michael Kenealy, Mint Asset Management senior analyst, said he wasn’t surprised at the popularity of the longer terms.

“People are stretching their budgets as much as they can, and digging into their pockets as deep as they can, to buy,” Kenealy told Stuff.

He said borrowers struggling to keep up with repayments in the past could extend the term of their loan, but this option was being eroded for some.

While extending a mortgage meant borrowers took longer to pay off the debt and reduced their immediate repayments, they also ultimately paid more in interest.

Read more: Homeowners face higher mortgage repayments

Mortgage stress is expected to rise along with interest rates, and in a worst-case scenario, could see some banks putting borrowers onto interest-only repayments for a period, or even reintroduce target mortgage repayment holidays, as they did at the start of the pandemic, Kenealy said.

He warned that allowing too much interest or debt forgiveness could result in moral hazard, meaning borrowers may become more willing to accept unreasonable risk because they felt protected from consequences.

Stuart Baxter, Centrix analytics general manager, said there were rare instances of home loans having terms above 30 years.

“It is not surprising to see longer term mortgages have been on the rise in the last year, as higher property prices and the recent rate hikes have squeezed borrower cash flows,” Baxter told Stuff. “Borrowers are being pushed into longer term mortgages to keep payments as low as they can so that they can meet their short-term budget.”

Despite the trend, Baxter believed it was unlikely 35- or even 40-year terms would rise.

“Considering the average age of a typical first-time buyer is in their mid-30’s, a 40-year term would take them well into their 70’s, which I think most banks would want to avoid,” he told Stuff.

Baxter said mortgage arrears and financial hardship remained at historically low levels.

“Responsible lending rules are designed to protect the most vulnerable borrower, but with the prospect of further rate hikes and higher costs of living in the months ahead, I think we will see more borrowers who find themselves under mortgage stress,” he said.

According to recent Reserve Bank analysis, a 5% increase in mortgage rates would see nearly 20% of recent first-home buyers facing serviceability stress. At 6%, this would be up to nearly 50%, with investors and some owner-occupiers would also be under pressure.

Kelvin Davidson, CoreLogic senior property economist, agreed increased prevalence of longer-term mortgages cut off a traditional method used by struggling borrowers to cope, Stuff reported.

Most vulnerable of the groups were recent entrants to the market, who had bought at the peak in November and December, and had gone in with only a 10% deposit, Davidson said.

The CoreLogic economist said the Reserve Bank was likely to continue to hike interest rates with inflation at a 30-year high.

“The housing market is going to be a little bit collateral damage because they simply have to get general inflation under control,” he said.

Read next: RBNZ's biggest hike in 22 years sounds inflation warning

Davidson said that while mortgage stress would increase as interest rates rise, unemployment remained low, which meant it was unlikely many homeowners would be forced to sell – which, consequently, made any kind of price crash unlikely.

“Really a lot hinges on the labour market; that’s where the stress could come from if we see job losses,” he said.

Davidson said there was a feeling in the sector that forced sales and mortgagee sales were undesirable for both lenders and borrowers, and banks would work with struggling homeowners.

RBNZ does not collect data on the proportion of home loans issued at different duration terms, which Davidson said could constitute a blind spot for the central bank, Stuff reported.