Why this originator says the Florida mortgage business is still strong

Christian J. Plocica (pictured) first studied as an educator, getting his Bachelor’s degree in Health and Physical Education at SUNY Cortland. And, at first, Plocica followed his chosen route – getting a job in the warmth – in Florida’s Seminole County Public School system. But after almost eight years teaching, he took the plunge into the mortgage pool.

Speaking to MPA, Plocica explained that his first mortgage job was as an originator – he joined Orlando-based The Mortgage Firm Inc, where he stayed until setting out after another eight years to help establish VIP Mortgage Group where he now acts as COO.

And, in Florida, where hurricanes are a fact of life, the real estate and mortgage industries have had to adapt to the unique challenges posed by these natural disasters and Plocica has plenty of firsthand experience dealing with these issues, especially when it comes to property damage claims.

“Anytime you have hurricanes, if there’s people that are currently under contract on a house, looking to buy a house... when FEMA declares devastation, the lender automatically puts a hold on the application,” he said.

Plocica explained that lenders require re-inspection of properties already appraised but potentially damaged by hurricanes.

“The appraiser has to go back out to the property to make sure no damages have been incurred,” he added. In his 12 years in the industry, however, Plocica noted that he hasn’t had a loan collapse due to hurricane damage, even though others in the state haven’t been as fortunate.

“I don’t recall the hurricane because… you become hurricane numb. When you live in Florida, you forget the names,” he said.

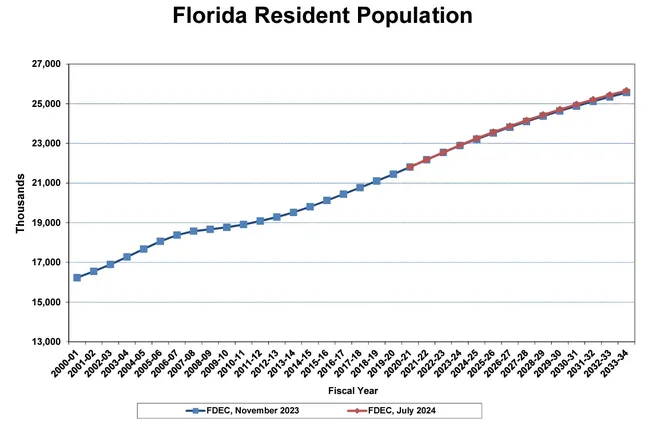

Despite these disruptions, people still flock to Florida, drawn by its lifestyle, weather, and lack of state income tax. As of April 1, 2024, Florida’s population exceeded 23 million, according to a state report, making it the third most populous state after California and Texas. “Florida is still going to be a hot spot,” Plocica said, noting that hurricanes don’t seem to deter most people from moving to the state. This marks a 15% increase since 2015, when Florida first hit 20 million residents. While deaths now outpace births, the state added over 358,000 new residents in 2023. That growth is expected to slow slightly, but projections still show the addition of over 300,000 new residents annually over the next five years.

In some ways, the state’s growth, despite its natural disaster risks, reflects a broader trend. “It’s not like these hurricanes just popped up this year,” Plocica pointed out. “You know what you get when you move into Florida.” While hurricanes may hit the coastlines, many people are moving inland, where the risk is lower. “If you don’t want to live on the coast, inland you’re going to be OK most of the time,” he said. And even when storms do come through, the state’s building codes, improved since Hurricane Andrew in 1992, mean that most homes are more resilient to storm damage than ever before.

That said, hurricanes do impact the housing market, especially in terms of availability. Plocica noted that in an already low-inventory environment, storms can temporarily take homes off the market. “If someone’s looking at a house, or let’s say a seller has a house and they’re looking to put it up for sale, and stuff happens, it’s going to take them longer to get the house ready,” he said. This further limits an already tight supply of homes, especially in high-demand areas.

Read more: Six effective tips to sell your house fast

Insurance is another hurdle. As hurricane activity continues, insurance premiums have skyrocketed, making homes less affordable. “Back in 2012, I would estimate about $1,500 for annual insurance. Now I’m starting estimates at $2,800 to $3,000 a year,” Plocica explained. This dramatic rise is pricing some buyers out of the market, especially as premiums increase debt-to-income ratios, disqualifying potential homeowners who would have otherwise qualified for loans just a few years ago.

Read more: Insolvency looms for Florida insurers

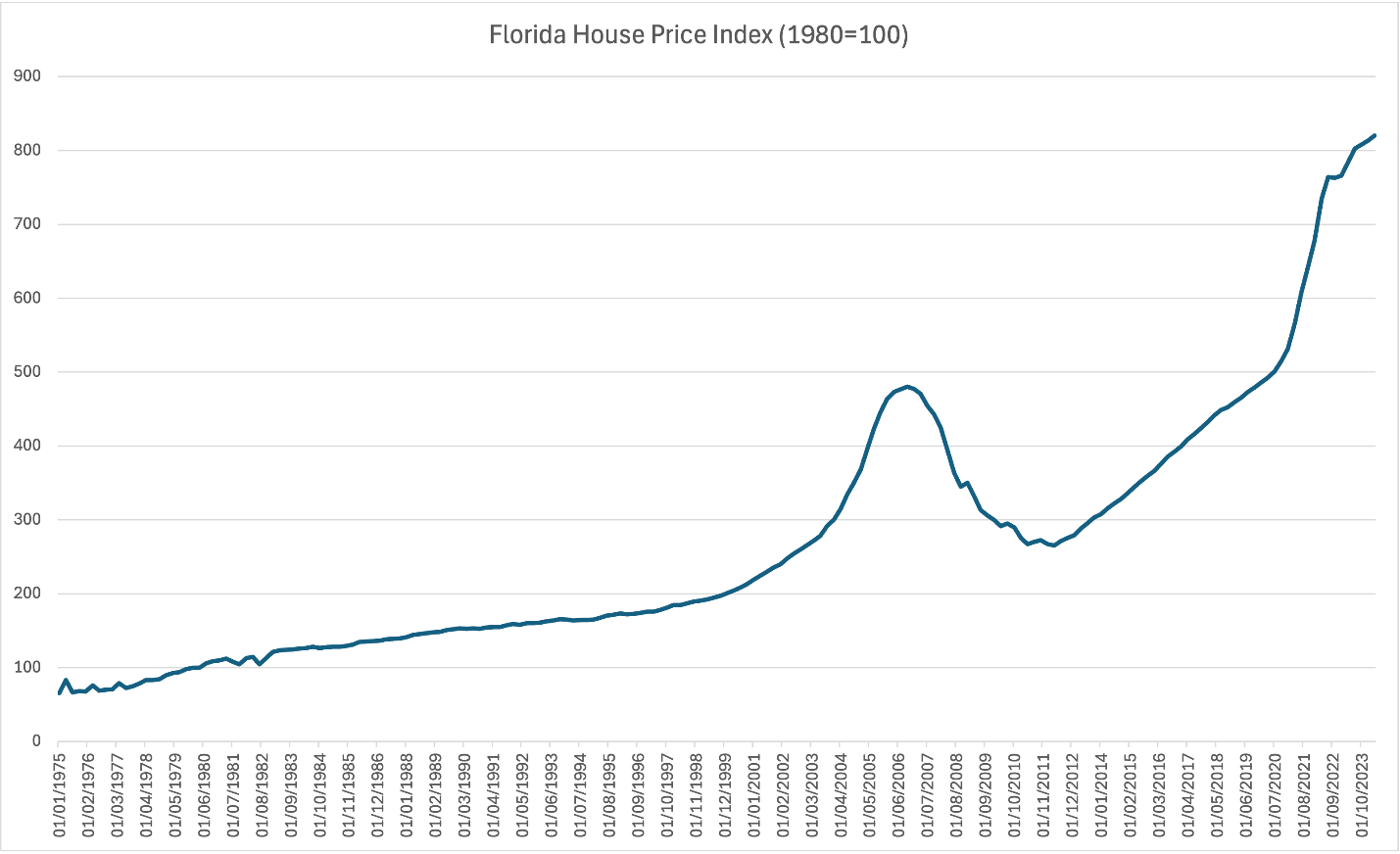

Beyond insurance, the state’s housing market faces additional challenges. Florida experienced a sharp appreciation in home values during the pandemic. Plocica observed that “normal appreciation stays three-five per cent a year. We had like 18-20% in a year.” Such rapid price increases have made homes less affordable, particularly for first-time homebuyers, whose wages haven’t kept pace with rising property values.

Plocica expects the situation to improve somewhat if mortgage rates come down, as that could help both homebuyers and lenders. He noted that there was a brief period recently when rates dropped, though they have since risen again due to market speculation. While he is hopeful that refinancing will pick up once rates decrease, he remains cautious about predicting exactly when that will happen.

Despite all these challenges, Florida’s appeal remains strong. Even in the face of natural disasters, rising insurance premiums, and a competitive housing market, the state’s population continues to grow, driven by people relocating from other states. This is especially true for retirees and families drawn by Florida’s lifestyle and the fact that, as Plocica put it, “there’s no state income tax.”

For Plocica, navigating the complexities of Florida’s housing market requires a team approach. He describes his role not just as a mortgage originator but as part of a broader financial advisory team that helps clients consider the full scope of their investment. “You have three hats. You originate the loan. You’re a financial advisor... but also you’re that therapist, right? They always have a lot of questions, and you’ve got to be the one to listen and hopefully give the best advice possible,” he explained.

Working closely with realtors is also essential, especially when assessing the risks associated with different areas. Plocica emphasized the importance of collaboration, noting that no one professional has all the answers. “We all work as a team, because there might be some things that I don’t know. Maybe outside of this area, which might be a high risk or low risk, they might have questions about the area,” he said.

The state’s population boom and continued appeal show that hurricanes, rising costs, and even insurance headaches aren’t enough to drive people away. “I don’t see people not coming to Florida anymore because it’s more of a higher risk,” Plocica said.

So just which counties of the US are most at risk?

These are the 20 most hurricane-vulnerable counties and their overall vulnerability scores according to Columbia’s NCDP (out of 100):

- Broward County, Florida, 72.70

- Palm Beach County, Florida, 72.09

- Charleston County, South Carolina, 68.17

- Horry County, South Carolina, 66.31

- Miami-Dade County, Florida, 65.10

- Beaufort County, South Carolina, 64.93

- Berkeley County, South Carolina, 62.76

- Chatham County, Georgia, 62.50

- Dorchester County, South Carolina, 60.97

- Onslow County, North Carolina, 60.75

- Brevard County, Florida, 59.98

- Georgetown County, South Carolina, 59.61

- Harris County, Texas, 57.89

- New Hanover County, North Carolina, 57.73

- Orange County, Florida, 57.02

- St. Lucie County, Florida, 55.83

- Florence County, South Carolina, 55.80

- Collier County, Florida, 54.98

- Carteret County, North Carolina, 54.74

- Volusia County, Florida, 54.55