While there is no set formula in calculating the cost of refinancing a mortgage, we’ll go over the basic fees in this article. Read on to find out more

The cost of refinancing a mortgage includes fees and expenses related to your current mortgage balance with a new one. Refinancing costs usually include most of the same fees you paid when you first closed on your home loan.

Keep in mind, however, that there is no set formula for calculating the cost of refinancing. Some are flat fees that differ from lender to lender. Others are based on a percentage of your loan amount. You also need to consider recurring closing costs that come with normal homeownership expenses, including property taxes and homeowners' insurance.

If you want to replace your current mortgage with a better one, you will need to pay attention to your estimated refinance closing costs. Knowing the full costs to refinance will help you determine if you are getting the best deal.

In this article, we will detail the cost of refinancing a mortgage. Before we get started, it might help to look at our guide on everything you need to know about refinancing.

What is the average cost of refinancing a mortgage?

The average cost of refinancing a mortgage, not including any taxes, is $2,375, according to ClosingCorp. However, when refinancing a mortgage, closing costs can vary widely depending on the size of your home loan, as well as the county and state you live in.

You will likely pay somewhere between 2% and 5% of the principal of the home loan in closing costs. For instance, closing costs would likely run anywhere from $4,000 to $10,000 on a mortgage refinance that costs $200,000.

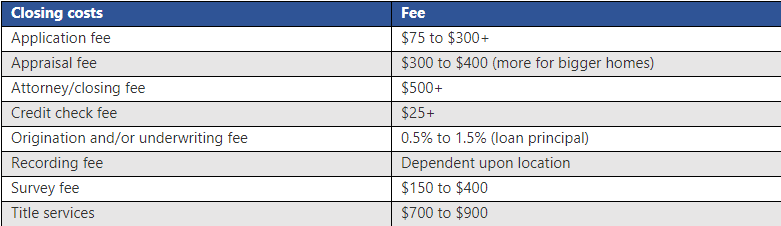

Let’s look at some of the costs included in refinancing a mortgage:

Cost of refinancing a mortgage: ways to save money

While there are numerous costs of refinancing a mortgage—and they do add up—there are also ways to save money. Let’s look at where you can save when refinancing:

- Boost credit score

- Shop around

- Negotiate

- Request fee waivers

- Consider buying mortgage points

- Opt for original title insurer

- Think about no-closing-cost refinance

Here is a closer look at each of the ways you can cut down on the cost of refinancing a mortgage:

1. Boost credit score

When you applied for your first mortgage, you aimed for a certain credit score. The same aim should apply when you refinance your mortgage also; you will need to meet credit score minimums to refinance. The stronger your credit score is, the lower your refinance rate will be. How do you boost your credit score? There are numerous strategies, chief among them paying off any debt or at the very least paying it down.

2. Shop around

In other words, you will want to compare mortgage rates and offers. To do this, you must compare offers from several mortgage refinance lenders and banks. To get a better sense of the cost of the loan, ensure you look at APR.

To get a range of offers, you can also consider working with a mortgage broker. Just be sure you get a quote from your current lender also. You may end up getting a lower-cost refinancing offer or other benefits for repeat customers.

3. Negotiate

To understand the precise cost of refinancing a mortgage, look closely at the loan estimate from your mortgage lender, just like you did with your first mortgage. If you negotiate closing costs, you may save yourself some money. This would be especially true if you shopped around and received more than one refinancing offer. To check for oddly high fees, you can use other quotes as well.

4. Request fee waivers

You can also ask your lender or bank for a waiver or lower credit check fee or application fee. You can request your lender to forgo a property survey, if you have had one completed recently, or to forgo a new home appraisal. If you are an existing client, your bank may be willing to work with you in these areas.

5. Consider buying mortgage points

Mortgage point, or discount points, may be one way to lower the cost of refinancing a mortgage. Buying these points may lower your interest rate, but they are best if you plan to own the home for the long-term and do not plan on refinancing again.

Find out more about mortgage points in our short explainer.

6. Opt for original title insurer

Title rates are regulated in many US states. However, you can try to cut down your title services costs. How? By asking your title insurance company how much money it would charge to reissue the policy for your refinance. This may cost less than starting over with a brand-new policy or mortgage company. And, if you did not get an owner’s policy for your first mortgage, you should consider getting one for your refinance.

7. Think about no-closing-cost refinance

A no-closing-cost refinance is a great option if you are low on money. While it is not free (as the name suggests), no-closing-cost refinance means you will not have to pay fees at closing. Lenders will instead raise your interest rate or include the closing costs into the new home loan.

Why are closing costs so high on a refinance?

Typically, closing costs range from 2% to 5% of the home loan amount. This amount includes third-party fees as well as lender fees.

Refinancing really means taking out a new loan to replace your old one. Because of this, you end up repaying many mortgage-related fees and costs. These usually include the loan origination fee, appraiser’s fee, credit report fee, application fee, and attorney fees, plus more.

These costs add up, making closing costs so high on a refinance. You may also want to pay additional fees like discount points to lower your interest rate.

Is there a way to avoid closing costs when refinancing?

There is no way to avoid closing costs when refinancing. You usually have to pay them somewhere. However, you can choose between two options with a no-closing-cost refinance:

- higher loan balance

- increased mortgage rates

Keep in mind that not all mortgage lenders offer both types of no-closing-cost refinances. It is therefore important to ensure beforehand that your lender can offer you the preferred option.

Let’s look more closely at each of the two no-closing-cost refinance options.

Higher loan balance

Your total loan balance increases when you decide to roll in your closing costs. Let’s say you are refinancing a loan of $150,000, for instance, with $5,000 in closing costs. This means your new balance, with closing costs included, will be $155,000.

Now, let’s look at the difference between a $155,000 refinance and a $150,000 refinance at an interest rate of 3.5%.

With a loan term of 15 years, your monthly payment would be roughly $1,072 for a refinance of $150,000. That includes principal and interest.

With a $155,000 refinance, on the other hand, your monthly payment for the same loan term will be about $1,108. This means the difference you will pay each month will be $36. However, you will also pay an extra $1,434 in interest for a $155,000 refinance compared to a $150,000 refinance, due to the higher balance.

However, the increase here is not as dramatic as taking a higher interest rate on the same amount, which we will look at now.

Increased mortgage rates

If your mortgage lender offers you a no-closing-cost refinance without adding funds onto your principal, you will have to accept a higher interest rate.

An increased mortgage rate does not alter your principal loan amount. However, you will pay significantly more in the long run if there is a small change in your interest rate.

For example, if you refinance your home for $150,000 over a 15-year term at 3.5% interest, your closing costs would typically be between 2% and 6% of your total loan amount. With closing costs at around $6,000, and at that interest rate, you will pay just over $43,000 in interest over the course of the refinance. When closing costs are added, you are looking at something closer to $49,000.

Cost of refinancing a mortgage: closing thoughts

If you want to refinance your mortgage, knowing the cost of refinancing a mortgage is an important first step. Understanding where these costs come from, and ways that you can lower those costs, are also critical in securing you the best refinancing option.

Remember: the more knowledge you have, the better off you will be.

For help in getting the best deal when refinancing your mortgage, get in touch with one of the mortgage professionals we highlight in our Best of Mortgage section. Here you will find the top performing mortgage professionals across the USA.

Did you find these tips useful? Do you have experience lowering the cost of refinancing a mortgage? Let us know in the comment section below.