Despite sweeping changes at Fannie Mae and Freddie Mac, FHFA Director Bill Pulte confirms the agency will maintain current lending thresholds

The head of the Federal Housing Finance Agency (FHFA) has confirmed that the conforming loan limits for 2025 will remain intact, offering stability in an otherwise volatile period for the nation’s housing finance system.

“There are no plans to do anything as it relates to the conforming loan limit,” FHFA Director Bill Pulte said this week, signaling a pause on changes to one of the agency’s most closely watched levers.

The conforming loan limit—the maximum size of a mortgage that Fannie Mae and Freddie Mac can purchase—has been set at $806,500 for 2025. That figure, which applies to most of the United States, represents a 5.2% increase over last year, consistent with the growth in average U.S. home prices tracked by the agency’s house price index.

While the loan ceiling in high-cost markets such as parts of California and New York can rise as high as $1,209,750, this year’s adjustments follow a statutory formula outlined in the Housing and Economic Recovery Act of 2008 (HERA), tying the limits to national price trends.

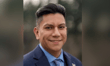

Pulte, a home-building scion and newcomer to public service, was recently confirmed as FHFA director under the Trump administration. His short tenure has already seen dramatic changes, including a purge of top executives at Fannie Mae and Freddie Mac and a reshuffling of their boards of directors. Pulte appointed himself chairman of both entities before the abrupt resignation of one of his new appointees, entrepreneur and Musk confidant Christopher Stanley.

Despite the leadership churn, Pulte appears intent—at least for now—on keeping certain housing market parameters steady. That includes the conforming loan limits, which directly affect the size and cost of mortgages accessible to middle- and upper-middle-income borrowers.

Both Fannie and Freddie have been under government conservatorship since the 2008 financial crisis. They support roughly $12 trillion in the U.S. mortgage market by purchasing loans from lenders, bundling them into securities, and guaranteeing investors against losses from borrower defaults.

The Trump administration has revived efforts to reduce the federal footprint in housing finance. Long-held Republican goals to privatize Fannie Mae and Freddie Mac are reportedly back on the table. According to sources familiar with the matter, discussions have included transferring Treasury’s stake in the companies to a potential sovereign wealth fund—a novel idea floated by Treasury Secretary Scott Bessent on a recent podcast.

Some analysts estimate the government’s share of the two firms could be worth over $250 billion, positioning the plan as a potential windfall in an era of mounting federal deficits. However, critics warn that pushing the firms into private hands too hastily could rattle the mortgage-backed securities market and push up home loan rates.

“There’s a lot of pressure on a pretty unseasoned board and management team,” said Moody’s chief economist Mark Zandi, noting that while the U.S. economy remains stable for now, an economic downturn could quickly test the new leadership’s capacity.

Inside the FHFA, the pace of change has also been jarring. According to the National Treasury Employees Union, dozens of staff have been placed on indefinite administrative leave, some notified in makeshift meeting rooms, including an unused cafeteria space.

Pulte, who has been highly active on social media, shared footage of empty workstations during a recent visit to agency offices. “There are some really great people inside of these businesses, and the good news for them is there is a lot of upward mobility, to earn and grow MORE!” he posted on X.

While the FHFA has remained silent on the broader shake-up, concerns are emerging that internal disruptions could impact key regulatory functions, from fair-housing oversight to mortgage pricing. A top bank regulator warned that technical glitches or pricing missteps—even if minor—could erode investor confidence in mortgage-backed securities and push borrowing costs higher.

In this uncertain environment, maintaining the conforming loan limit offers one point of continuity. The CATO Institute, a libertarian think tank, has advocated for tighter restrictions on government-backed lending, urging that the FHA and GSEs focus more narrowly on first-time homebuyers and lower-priced homes.

But for now, that vision is not shared by the FHFA’s new leader—at least not publicly. With house prices continuing to rise in most of the country, and with few signs of a slowdown, the decision to keep the current loan limit in place may offer temporary reassurance to lenders, borrowers, and investors alike.

As the Trump administration explores transformative moves in housing finance, the preservation of existing loan thresholds underscores the delicate balancing act between ideology and market stability.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.