The market's current state has led to a wave of consolidation, warns branch manager

Loan officers across the US are waking up to the tough times our sector is experiencing. Dave Thomas, branch manager at Union Home Mortgage, told MPA that the current crisis is more severe than the 2008 crash, despite having a more extensive client base now.

“I know a lot of people are transferring companies right now based on the market and the environment of mortgage,” he explained. “I would say that 2008 crash was easier than what we're going through now – and this is with a significant amount more of clients.”

Thomas’s commitment to his clients even extends to their friends and their families – something that saw him, in the 11 years prior with NewRez, fund nearly $1 billion in loans.

“I'm now doing loans for their kids, and their kids' kids,” he added.

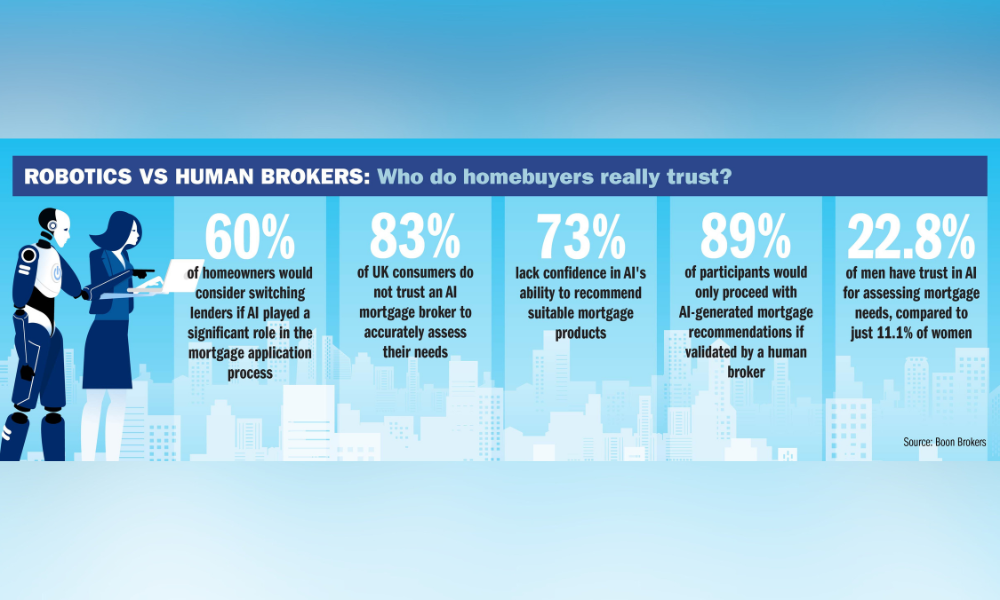

Thomas has managed to maintain these personal connections even in the face of rising digitization and an increasing reliance of AI in the sector. According to research from Fannie Mae, 65% of lenders are familiar with AI, yet only seven per cent (7%) have currently deployed it in some form – suggesting that both lenders and their clients are keen to hold on to that human touch.

“I love my clients. I love the face-to-face. I love the relationship aspect of it,” said Thomas. This human element, he believes, is irreplaceable, even as technology, like AI, becomes more prevalent.

The market's current state has led to a wave of consolidation, which Thomas compares to the banking crisis of 2008-2009. He points out that many loan officers and realtors are struggling to maintain their lifestyle due to the lack of business.

“How do you convince that client that's got their house at, let's say, three and a half per cent...to get you in another house here at 6.99%?” Thomas questioned. However, he also identifies consolidation as both a challenge and an opportunity.

“You get rid of a bunch of mortgage companies or they get acquired,” he said. “The loan officers that are good are working hard. They’re staying positive, they're staying in it. But these other companies have a large opportunity right now to take loan officers who are stressed. They can pick up and pluck some of these loan officers from different companies and build up. It's almost like acquiring another company.”

And Thomas is acutely aware of the need for adaptability in this evolving market. With inventory issues and a lack of new listings, he has expanded his licensing to 31 states, targeting markets with lower costs of living. This adaptability is not about aggressive sales tactics but about genuinely helping clients.

“I need to make sure I'm taking care of those clients because, if you do the right thing, they will come back to you,” he adds.

Looking ahead, Thomas sees potential for a positive shift in the market. He advises loan officers to prepare now by organizing their databases and staying in touch with clients.

“You don't want to be a month behind when it hits,” he warned. He also emphasizes the importance of the human touch, even as AI and technology become more integrated into the industry. “People still want that human there,” he said.

Despite the ongoing market challenges, Thomas is optimistic and proactive in his outlook for the future. He encourages loan officers to stay positive and reach out to clients and colleagues, even in tough times.

“Be available. Talk to people all the time. Be positive out there because it's a hard market for people,” he advised.