Report reveals positive impact of rising home prices on homeowners

A new CoreLogic report shows that surging home prices over the past year have helped lift millions of homeowners out of negative equity, providing a solid financial cushion.

According to CoreLogic’s latest Homeowner Equity Report, homeowners with mortgages saw their equity increase by 8.6% year-over-year in Q4 2023 – a collective $1.3 trillion gain averaging over $24,000 per borrower. This brought total homeowner equity to $16.6 trillion.

Home price growth helped significantly reduce the number of borrowers who were underwater on their mortgages. Slightly more than one million homeowners remained underwater by year-end, the lowest level in CoreLogic’s historic data and a sharp drop from 12 million coming out of the Great Recession.

The surging equity provides a major financial buffer, especially for longer-tenured owners like baby boomers who have accumulated substantial housing wealth over time.

“Rising home prices continue to fuel growing home equity, which, at $298,000 per average borrower, remained near historic highs at the end of 2023,” CoreLogic chief economist Selma Hepp said in the report. “By extension, at 43%, the average loan-to-value ratio of US borrowers has also remained in line with record lows, which suggests that the typical homeowner has notable home equity reserves that can be tapped if needed.”

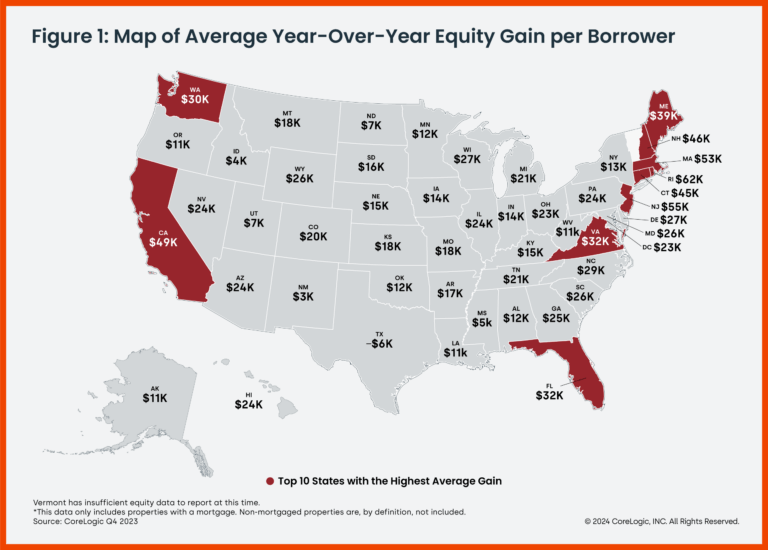

States like Rhode Island, New Jersey, and Massachusetts saw the highest annual equity gains, exceeding $50,000 per borrower on average.

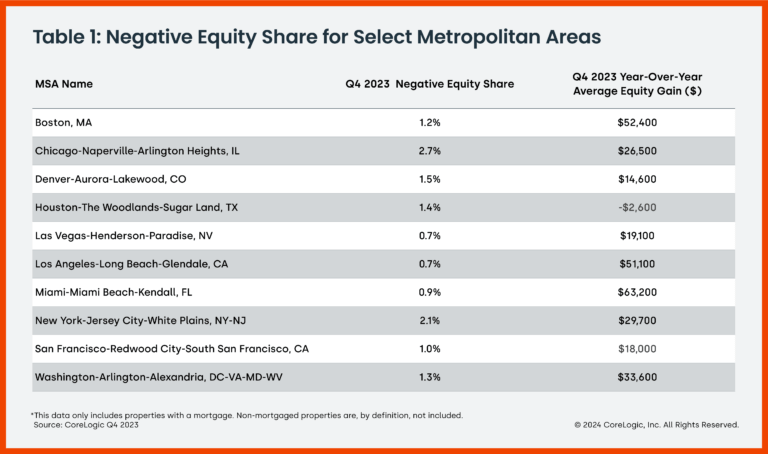

The report also addressed negative equity, with the total number of mortgaged homes in negative equity decreasing by 1.1% from the third quarter to the fourth quarter of 2023. On an annual basis, the number of homes in negative equity dropped by 15% from the fourth quarter of 2022 to the fourth quarter of 2023.

Read next: Mortgage rate lock activity increases

Considering the impact of home price changes, borrowers with equity positions near the negative equity cutoff were most likely to transition in or out of negative equity. For instance, if home prices increased by 5%, approximately 114,000 homes would regain equity, while a 5% decline in home prices would result in 162,000 properties falling underwater.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.