Stable refinancing activity buoys lenders' profitability outlook despite coronavirus crisis

Mortgage lenders' profit expectations for the next three months dipped in the second quarter but remained positive due to strong refinance demand.

Around 52% of senior mortgage executives in the Fannie Mae Mortgage Lender Sentiment Survey look forward to higher profit margins. Meanwhile, 24% believe profits will stay the same, and 23% expect profits to drop.

Despite the decline, mortgage spreads remain high – consistent with lenders' profitability expectations. The average primary mortgage spreads (FRM 30 contract rate versus 10-year) rocketed to 256 basis points in May, up from the long-run average of 168 basis points.

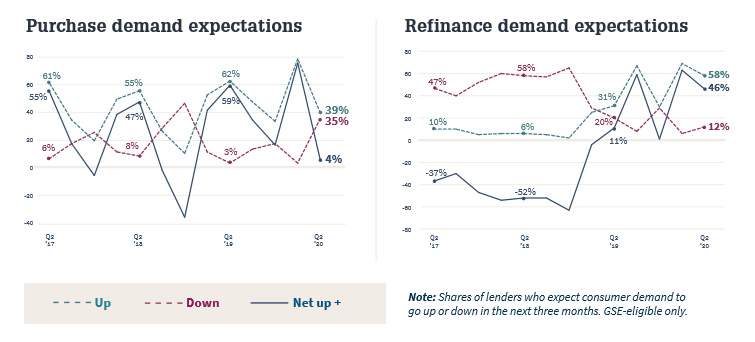

Across all loan types, demand for purchase mortgages for the past three months, and the next three months posted a significant decline. Non-GSE-eligible mortgages plummeted to their lowest reading since survey inception. The sharp drop indicates a shift toward the GSE-eligible lending market, according to Fannie Mae Chief Economist Doug Duncan.

"This quarter's results reflect the impact of COVID-19 on all fronts," he said. "Lenders attributed the purchase mortgage demand decline to COVID-19-related factors, including home price uncertainty, higher unemployment, policy changes, and lower inventory. Lenders pointed to the same reasons for credit tightening."

However, some encouraging signs have kept lenders' hopes afloat amid the coronavirus economic freefall, according to Duncan.

"For the agency lending market, the purchase demand outlook remains positive on net and is well above the Q4 2018 reading, a period of accelerated declines," he said. "If borrowers perceive the bottom of the economic downturn as having passed, there could be a pickup in purchase demand to take advantage of continued low mortgage rates."

Demand growth for refinance mortgages over the prior three months hit its peak for GSE-eligible loans. The net share of lenders reporting demand growth for the next three months decreased last quarter but remained high across all loan types.

"Additionally, this quarter, refinance demand expectations held relatively stable, demonstrating continued strength," Duncan said. "Lenders' profitability outlook remains positive, likely because of stable refinance demand, lender capacity constraints, and still-wide mortgage spreads. Nevertheless, challenges remain as the uncertainty around COVID-19 persists, in particular for mortgage servicing."