Credit availability hits five-month low

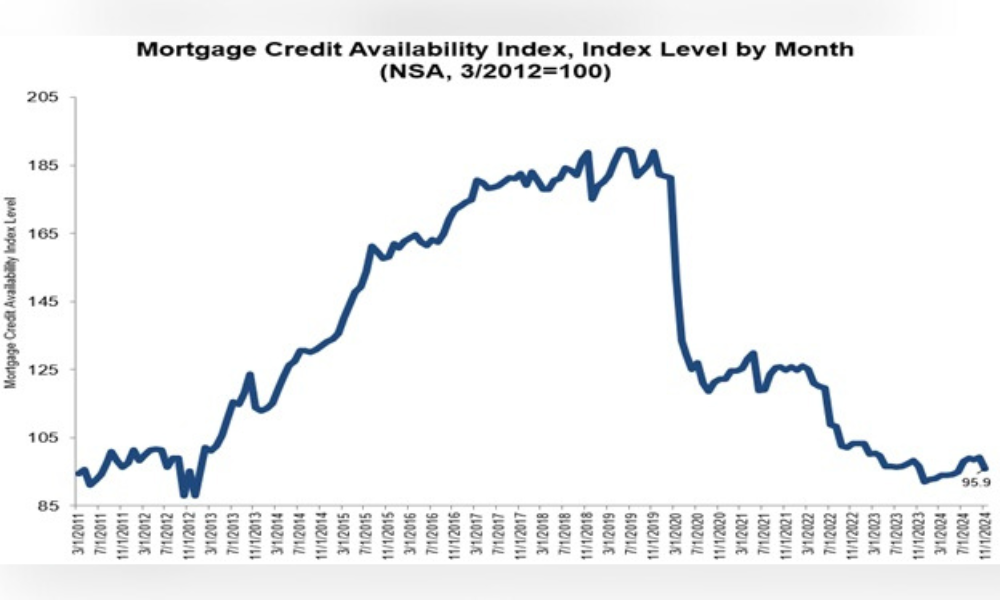

Mortgage credit availability tightened in November, hitting its lowest point in five months, according to the Mortgage Credit Availability Index (MCAI) from the Mortgage Bankers Association (MBA).

The index fell by 3.3% to 95.9, reflecting increasingly restrictive lending conditions. The MCAI tracks credit conditions using data from ICE Mortgage Technology. A decline in the index indicates stricter credit standards, while an increase suggests more flexibility. The index is benchmarked to 100, based on conditions in March 2012.

Tightening across the board

Government-backed lending saw the most significant contraction, with the Government MCAI decreasing by 3.9%, marking its lowest level since December 2012. Conventional credit availability also shrank by 2.7%, with the jumbo segment falling 0.9% and the conforming segment dropping 6.6%.

“Credit availability tightened considerably in November, pushing the index to the lowest level in five months,” Joel Kan, MBA’s deputy chief economist, said in the report. “Part of the decline was attributable to investors pulling back on high LTV and low credit score programs for both fixed and ARM loans, as well as further exits from the broker channel in an originations market that is still challenging for many lenders. The most notable impact was on the government index, which decreased to its lowest since December 2012.”

FICO price hike adds to concerns

The tightening credit conditions coincided with the price increase from Fair Isaac Corp. (FICO), which raised its wholesale royalty fee for mortgage-related credit scores by 41%, from $3.50 to $4.95 per score.

Jim Wehmann, FICO’s executive vice president, clarified the company’s role and the breakdown of costs. According to Wehmann, FICO’s royalty accounts for roughly 15% of the total cost of a tri-merge credit report bundle, which typically ranges from $80 to over $100.

The price hike, effective for 2025, has sparked concern among mortgage professionals, who warned of potential cost increases for lenders and consumers.

Read more: FICO credit score price hike: What does it mean for the mortgage industry?

“MBA remains deeply frustrated by the annual price hikes for tri-merge credit reports and other credit reporting products,” MBA president and CEO Bob Broeksmit said. “Lenders are required by the government to obtain FICO scores and three credit reports to make most loans.

“It is troubling that these providers have the audacity to use their oligopoly powers to raise prices at many times the pace of inflation during this time of constrained housing affordability.”

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.