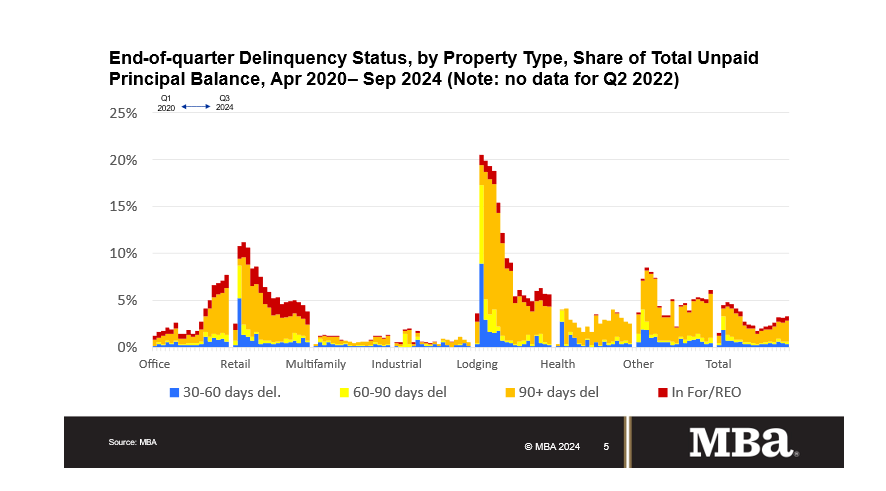

Lodging, retail, and industrial loans see improvement

Delinquency rates for commercial mortgages saw a slight overall increase during the third quarter of 2024, driven by rising delinquencies in loans backed by office properties.

By the end of the third quarter, 96.8% of all outstanding commercial loan balances were current or less than 30 days overdue, down slightly from 97% in the previous quarter.

Loans that were 90 or more days delinquent, or classified as real estate owned (REO), rose to 2.7% from 2.5% the previous quarter. Loans that were 60-90 days delinquent increased to 0.3% from 0.2%, while loans that were 30-60 days late declined to 0.3% from 0.4%.

"Delinquency rates for commercial mortgages backed by office properties continued to increase during the third quarter but declined for loans backed by lodging, retail and industrial properties,” said Jamie Woodwell, head of commercial real estate research at MBA.

He emphasized that the commercial mortgage market is highly varied, with performance influenced by the different property types, geographic locations, and economic factors.

Office property loans experienced the most significant delinquency increase, with 7.8% of the total loan balance 30 or more days delinquent, up from 7.1% in the previous quarter. The office sector continues to face significant challenges, with rising vacancies and a slow return to office spaces creating financial strain for property owners.

In contrast, loans backed by lodging, retail, and industrial properties fared better in Q3. The delinquency rate for lodging loans decreased slightly to 5.6%, down from 5.8%. Retail property loans saw a more substantial improvement, with delinquencies falling to 3.8% from 4.5%. Industrial property loans continued to show resilience, with only 0.6% of loans in this sector delinquent, down from 0.8% in Q2.

Multifamily loans saw a minor uptick, with the delinquency rate rising to 1.2% from 1.1% in the previous quarter, indicating relatively stable performance.

“Each of those differences is affecting loan performance, some to the good and some to the bad,” Woodwell said in the report.

Commercial Mortgage-Backed Securities (CMBS) loans remained the most delinquent among major capital sources, with 4.8% of loan balances 30 days or more overdue—unchanged from the previous quarter.

Read next: Commercial real estate turbulence not easing yet - exec

Other capital sources, including loans backed by life insurance companies and government agencies, showed mixed results. FHA multifamily and healthcare loans held steady at 0.9% delinquent, while life company loans saw a slight improvement, with delinquencies dropping to 0.9% from 1.0%. Meanwhile, GSE-backed loans experienced a small increase in delinquencies, rising to 0.5% from 0.4%.

MBA’s report, based on data from $2.6 trillion in commercial and multifamily loans, representing 56% of the total outstanding loan debt in the sector, offers a snapshot of the varying performance across property types and capital sources.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter