Better borrower profiles has reduced the risk of non-QM loan defaults

Non-qualified mortgages (non-QM) are gaining ground in the mortgage market, as these loans, once seen as risky, have become a safer option for many borrowers, according to a new report from CoreLogic.

The non-QM market, which saw a sharp decline during the pandemic, dropped to less than 3% of total mortgage originations in 2020. However, by 2022, the non-QM market had nearly doubled, reaching about 5% in 2024.

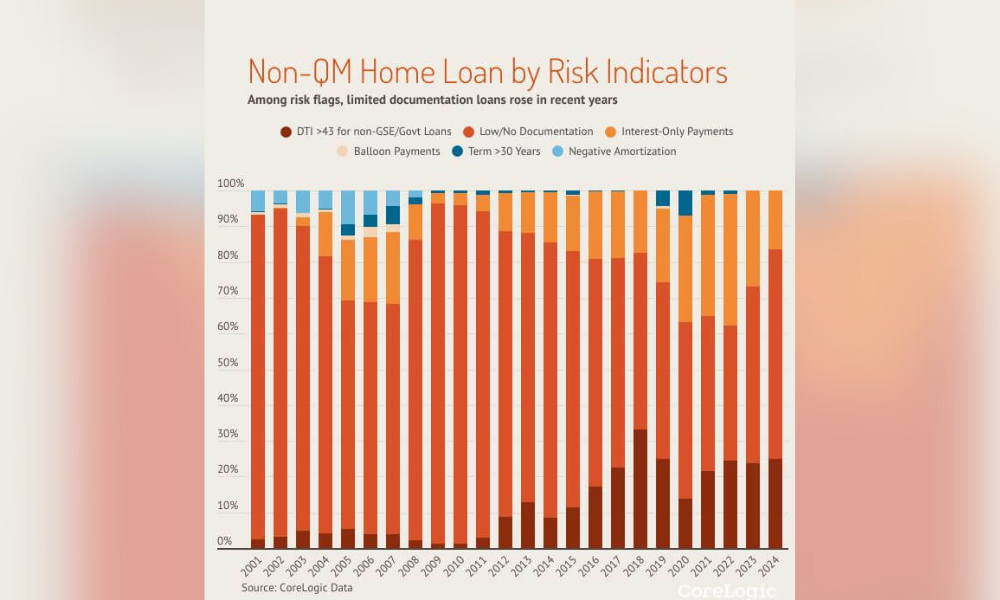

Non-QM loans do not meet at least one of the criteria set by Qualified Mortgage (QM) standards, such as having a maximum debt-to-income (DTI) ratio of 43%, or full documentation of income. The primary reasons non-QM loans fell outside QM standards in 2024 included the use of limited or alternative documentation (62%), mortgages with DTI ratios exceeding 43% (26%), and interest-only loans (17%).

The report highlighted that the structure of non-QM loans has shifted since 2020, with the share of interest-only loans dropping by nearly half, while the proportion of loans with DTI ratios over 43% increased by 12 percentage points. Meanwhile, riskier features such as negative amortization and balloon payments have been eliminated.

In terms of borrower quality, non-QM loans are now performing similarly to QM loans in many respects. For example, the average credit score for non-QM borrowers in 2024 was 776, compared to 781 for conventional QM loans, and 699 for government-backed loans. The loan-to-value (LTV) ratio was also comparable between non-QM and QM loans, both averaging 75%, while government loans had a higher LTV of 97%.

While non-QM borrowers often have higher DTI ratios, the report noted that these loans are still performing well, with delinquency rates significantly lower than those for government loans.

Higher rates, lower risk

To offset the higher risk of default associated with non-QM loans, lenders generally charge slightly higher interest rates.

In 2024, the average 30-year mortgage rate for non-QM loans was 6.7%, compared to 6.4% for QM loans. However, lenders are focusing on higher credit scores and lower LTV ratios to balance out the inherent risks associated with high DTI ratios, limited documentation, and interest-only features.

Read next: Execs talk non-QM growth among Hispanic borrowers

Despite these risks, non-QM loans play a crucial role in the mortgage market.

“These loans provide a valuable option for creditworthy borrowers, including self-employed individuals, gig economy workers, first-time homebuyers, borrowers with significant assets but limited income, jumbo loan borrowers, and investors,” CoreLogic principal economist Archana Pradhan wrote in the report.

Since the introduction of the Qualified Mortgage rules in 2014, which followed the Dodd-Frank Act, lenders have had to comply with the Ability-to-Repay (ATR) rule. This ensures that borrowers have the capacity to repay their loans, while non-QM loans must meet certain requirements, even if they don’t adhere to all QM standards.

Stay updated with the freshest mortgage news. Get exclusive interviews, breaking news, and industry events in your inbox, and always be the first to know by subscribing to our FREE daily newsletter.