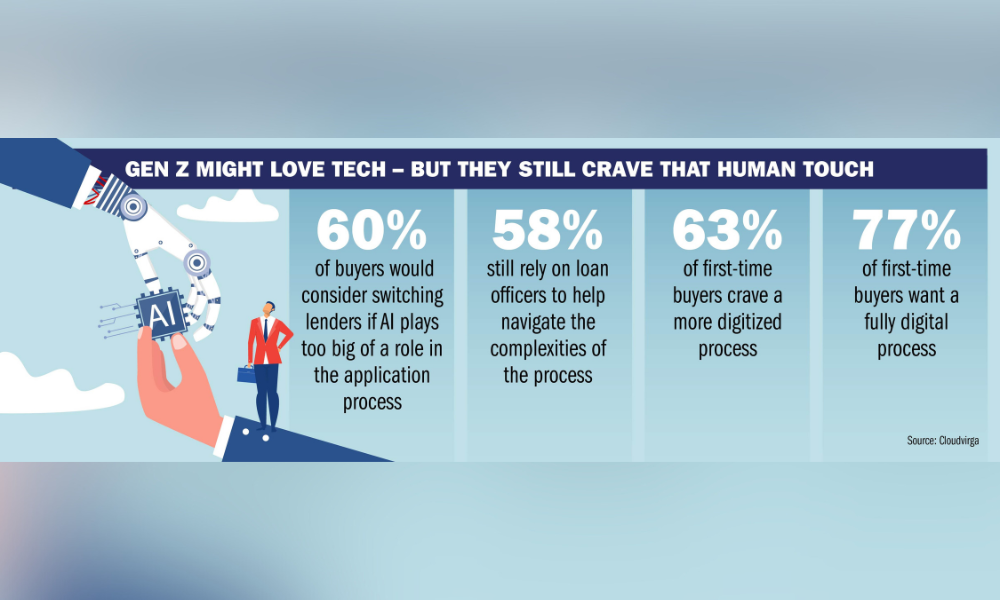

It's a case of adapt or fall behind when it comes to emerging tech

Embracing technology is no longer optional for mortgage originators—it’s essential to thrive in a competitive and evolving industry. Research from ICE found that 90% of lenders believe technology does enhance the application process, with 74% adding it simplifies the process, 70% adding it reduces closing times, and 67% believing it minimizes data entry.

And, historically focused on sales, “originators now must act as CEOs, balancing key pillars: finance, sales, marketing, and operations. Technology has become vital in this structure, second only to people,” Delightful Refuge’s Stacia Weishaar (pictured) told MPA. Modern consumers expect instant, seamless service, requiring originators to move beyond the antiquated systems that dominate the industry.

“Customers expect things at the tap of a button,” Weishaar explained. “They expect information quickly.”

The existing loan origination systems (LOS), is “antiquated and terrible,” Weishaar explained, highlighting the need for better solutions. Advanced technology enhances efficiency, improves customer experiences, and positions originators for long-term success in a field where technological integration is no longer a choice but a requirement.

In that vein, Weishaar revealed the top seven types of technologies that originators should be embracing – and warned of some trends that should be avoided.

- AI-Powered Underwriting

AI algorithms can assess borrower risk more accurately and quickly than traditional methods, using a combination of credit data, alternative data sources, and predictive analytics to deliver faster, more accurate underwriting decisions.

“I have absolutely nothing but positive things to say about this,” explained Weishaar. “The thing about generative and analytical AI it's still not perfect - yet anybody who thinks that AI is not already used especially on agencies loans, to assess risk when they're running the quote, unquote decision engine, is kidding themselves. It's already there. It's been there for a long time.”

- Blockchain

Blockchain can enhance the security and transparency of mortgage transactions by providing a decentralized and tamper-proof ledger.

“Cryptographically wrapped data is going to be critically important, and will continue to be critically important, it will 100% come into play,” added Weishaar. “With some deregulation happening potentially, I think this cryptographic behavior and ability for AI to come into play will continue to enhance our ability to protect consumers data.”

- AI Processing

Using optical character recognition (OCR) and natural language processing (NLP), mortgage originators can automate the reading, categorizing, and verifying of mortgage application documents.

“As long as the of the application, the story, is told properly, we can leverage technology to create efficiencies. However, we must remember the importance of humans reviewing the data, you can put anything in an application and trick software, including AI, to provide a decision,” explained Weishaar. “Anybody can increase the income and all of a sudden I have an approval. There has to be some sort of human component to it, because I don't think that we are in a place that’s sophisticated enough to completely analyze an application and ensure there's no falsification or misinformation in there.”

- Virtual Assistants and Chatbots

AI-driven chatbots can handle routine inquiries, pre-qualify leads, and assist borrowers with status updates on their applications, providing 24/7 support.

“Very applicable and relevant, consumers are very comfortable with chatbots,” added Weishaar. “Virtual assistants, whether you believe it or not, are in your phone, in your calendar, in your Microsoft Office. And they'll be more and more prevalent, even if you're not paying extra for an AI virtual assistant.”

- Robotic Process Automation (RPA)

RPA can automate repetitive tasks, such as data entry, document verification, and compliance checks, which significantly reduces manual labor. This speeds up processing times, minimizes errors, and allows human resources to focus on higher-value activities like customer service and relationship management.

“Operational efficiencies and leveraging AI, such as managing data, managing inputs of data, analyzing data is super important,” added Weishaar. “And I do agree that it does allow for the origination team and processing team of the loan, to connect with their clients and manage their overall business.”

- AI in CRMs

“I think this is a big one,” explained Weishaar. “I think that anywhere we can integrate artificial intelligence, generative and analytical into a CRM system, it allows for much more lift, not only for the client's experience but it also allows originators to very quickly manage, sort and understand data and then communicate effectively and efficiently. Any CRM that doesn't have some level of AI employed in it is going to be obsolete.”

- Predictive analytics

By leveraging AI to analyze historical data and external market trends, predictive analytics can help originators identify potential borrowers who are more likely to convert.

“I don't think AI is going to tap into human emotional response mechanism to understand what is important from a buying perspective,” added Weishaar. “Can AI look at analytical behavior on like relocations? Can it look at how long someone has owned their current home, it can they look at like birth certificates, death certificates? Can it predict things in that perspective? Yes. Can that help originators move the needle on a transaction? Absolutely. It allows for humans to anticipate and understand patterns and possible roadblocks. But AI will not deeply understand the emotional component, the human perspective.”