Will next week's RBA cash rate decision hold surprises?

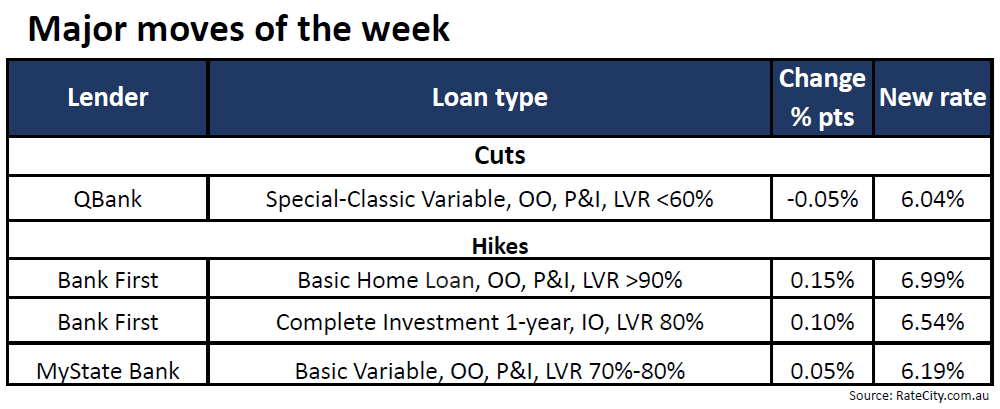

Mortgage rates remained largely unchanged this week, with only three lenders adjusting their fixed or variable rates, financial comparison website RateCity.com.au has reported.

Bank First increased both fixed and variable rates by up to 0.15 percentage points, MyState raised its basic variable rate by 0.05 percentage points, and QBank reduced a range of variable rates.

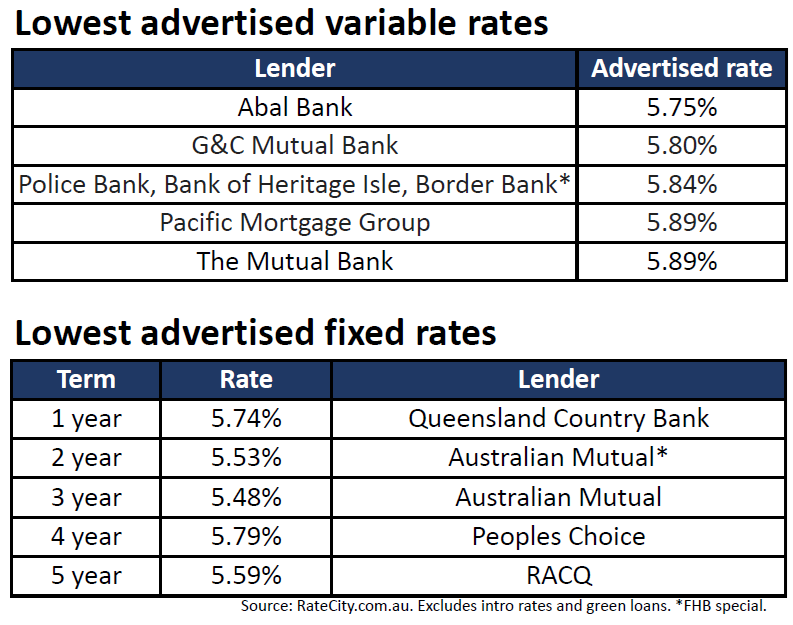

The lowest advertised fixed rates are led by Queensland Country Bank with a one-year term at 5.74%, while Australian Mutual offers the lowest rates for two- and three-year terms at 5.53% and 5.48%, respectively. Peoples Choice has a four-year fixed rate at 5.79%, and RACQ offers a five-year term at 5.59%.

Abal Bank has the lowest advertised variable rate at 5.75%, followed closely by G&C Mutual Bank at 5.80%. Police Bank, Bank of Heritage Isle, and Border Bank offer a rate of 5.84%, while Pacific Mortgage Group and The Mutual Bank both have rates at 5.89%.

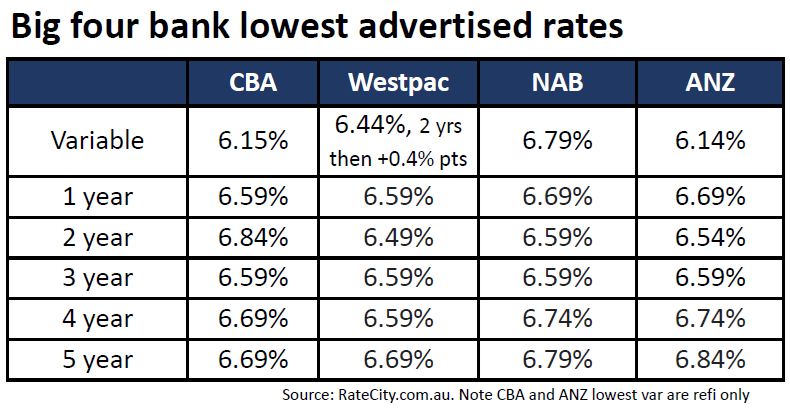

Meanwhile, the lowest advertised variable rates among the big four banks are as follows: CBA at 6.15%, Westpac at 6.44%, NAB at 6.79%, and ANZ at 6.14%.

Fixed rates for one-year terms are uniformly set at 6.59% across the big four. For two-year fixed terms, rates range from 6.49% at Westpac to 6.84% at CBA. The three-year fixed rates are consistent at 6.59% for all four banks.

Four-year fixed rates are set at 6.69% for CBA and 6.59% for Westpac, with NAB and ANZ both at 6.74%; while five-year fixed rates are 6.69% for CBA and Westpac, 6.79% for NAB, and 6.84% for ANZ.

“The latest APRA Quarterly Property Exposure Statistics out this week show the vast majority of home loan customers are managing to cope under higher rates,” said Sally Tindall (pictured), research director at RateCity.com.au. “The value of home loans that are 90 days or more past their due date rose for the fifth consecutive quarter, however, as a share of all outstanding mortgages. it represents just 0.95%.

“While this is still relatively low, particularly given the cash rate has risen 4.25 percentage points in the last two years or so, it is now higher than the 2019 pre-COVID arrears rate which was, on average, 0.91%.”

Tindall added that the proportion of mortgages on interest-only terms remains low, with interest-only lending accounting for 10.8% of the value of all outstanding mortgages, down from 11.3% before the rate hikes – indicating that borrowers are not moving to interest-only contracts en masse to manage the hikes.

She also pointed out that the value of loans approved as exemptions to serviceability requirements is up 64% from the same time last year but has declined from the previous quarter – suggesting that the wave of borrowers escaping ‘mortgage prison’ due to the banks’ reduced refinancing buffer is beginning to subside.

“Next week’s RBA board meeting is unlikely to include any major surprises, with the central bank set to keep rates on hold,” Tindall said. “Last meeting, Governor Bullock confirmed the board believes we could be at the cash rate peak, but it could not rule out the possibility of a further hike. It will be interesting to see if there is any change in language this time around.

“While all four big bank economic teams believe the next move to the cash rate will be down, ANZ has now split from the pack, saying the first cut won’t come til February 2025, while the other three still have November of this year pencilled in for the first cut. There’s a long way between now and November and a lot could change before then.”

Want to be regularly updated with mortgage news and features? Get exclusive interviews, breaking news, and industry events in your inbox – subscribe to our FREE daily newsletter. You can also follow us on Facebook, X (formerly Twitter), and LinkedIn.