After almost two years of ups and downs for Australia’s small business sector, lenders believe now is the time for brokers to reach out to SME customers as they prepare to move forward

At the start of October, Melbourne reached its 245th day in lockdown, bypassing Buenos Aires in Argentina as the most locked-down city in the world.

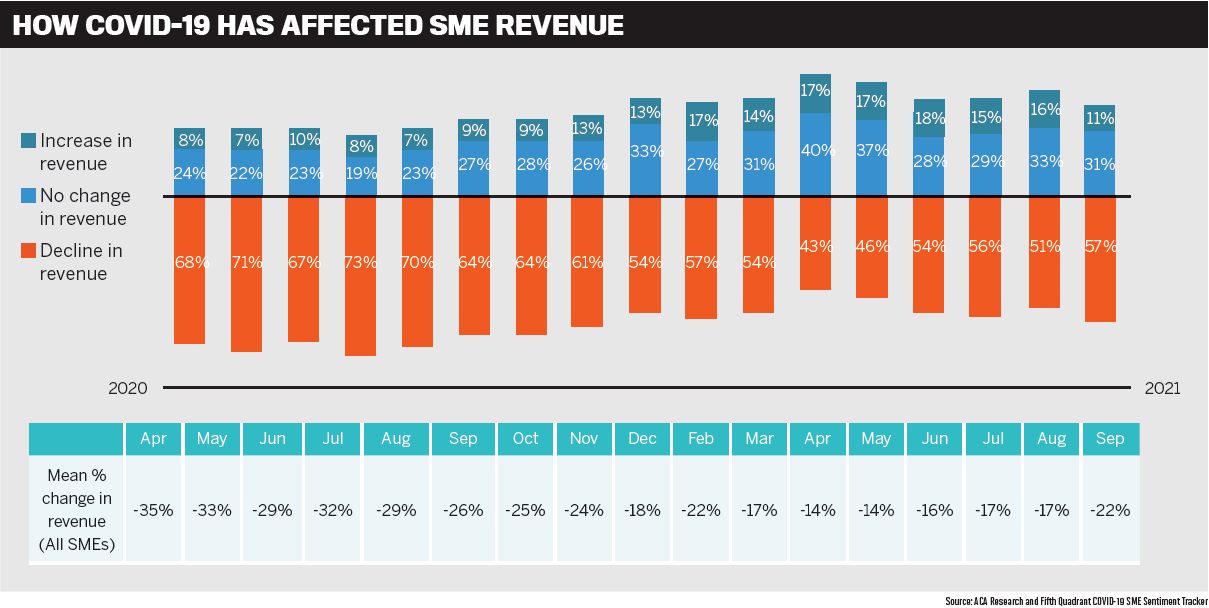

Small to medium-sized businesses have faced considerable challenges during the long period in lockdown. While many have managed to adapt to the restrictions, others have been forced to close completely for the entire duration.

According to the ACA Research and Fifth Quadrant COVID-19 SME Sentiment Tracker, more than half of all SMEs in Australia have reported a drop in revenue. Despite the lengthier Melbourne lockdowns, NSW businesses have reported the largest revenue losses.

Over the ups and downs and uncertainties of recent months, lenders have seen business needs shift. La Trobe Financial’s chief lending officer, Cory Bannister, says SMEs have responded in different ways: some have followed a defensive game plan, while others have gone on the offensive.

“A number of SMEs have really thrived during COVID, whether that’s through organic growth based on their particular industry being in demand, or in some cases as a result of them pivoting or slightly shifting in their business model, which has uncovered some opportunity,” Bannister says. He explains that these business owners have been looking for capital to grow.

“They can see the opportunity in front of them and want to lay those roots and foundations now, ready to capitalise that on the move out of this period.

“On the flip side, we’ve seen evidence of some severe stress, as you would expect, and some business owners that really have to play defence. They’re looking to restructure their commitments to get them through what’s a very challenging period, with the hope that once they get over that they can then start to rebuild from the other side.”

The stops and starts of the last year have affected SMEs and self-employed business owners because they have resulted in gaps in their income, Bannister points out. La Trobe Financial’s products, like its Lite Doc loans, have been designed to accommodate that, as well as other life events.

Alongside those great products, brokers are well placed to provide the right guidance and support to consumers.

“You never forget the people that helped you in times of need. So, for brokers, the appeal is that you’ve got the ability to create clients for life,” Bannister says. “Not only is it a great thing to do just to help people, which is what brokers do fantastically well, but it’s also an opportunity for them to help themselves and grow their portfolios.”

As brokers support those customers during the country’s reopening, Bannister says they will need to be compassionate and empathetic about what has been a significant life event.

Warning that the effects of the pandemic could continue to play out for some time, he adds that brokers need to keep in mind that it will not be “a light-switch moment”. When dealing with their customers they should look at their short-, medium- and long-term needs and wants, and work with them on future planning.

“We’re going to need to take a patient and cautious approach for a few months and perhaps years yet as the impacts of this play out,” Bannister says. “We would certainly encourage brokers to talk to lenders like us, and other NBFIs as well, to ensure they’re considering all options for SMEs.

“I think right now more than ever, complex credit is on the increase, and it’s going to need lenders that have got the capacity and the willingness to take the time and understand each individual situation and tailor a solution accordingly.”

Preparing to meet pent-up demand

Small business lender OnDeck saw a 175% jump in broker-originated loans from January to June 2021 compared to the year prior. Average loan sizes also increased by 20%.

National channel and partnerships manager Nick Reily puts much of this heightened activity down to the lender’s launch of KOALA Score, its innovative risk-predicting credit-scoring model which uses AI and machine learning. This has also enabled the group to introduce Lightning Loans, offering finance of up to $100,000 based on six months’ recent bank statements and no upfront asset security, approved in as little as two hours.

“As a leading online small business lender, OnDeck has always been about offering a unique best-in-class credit-scoring capability, understanding the needs of small business by providing better unsecured loan solutions. These unique capabilities are backed by a team that is passionate about small business,” Reily says.

Although the lockdowns over the last few months have caused a lot of stress and worry for small businesses, OnDeck is continuing to see increased demand, particularly in regional areas.

The jump in demand across the regions highlights that many enterprises are pivoting to take advantage of new products or services and new means of engaging with their customer bases during the pandemic, Reily says.

However, the lender’s research shows that small businesses often face an uphill battle to secure funds from mainstream banks. Of businesses that have applied for finance from a traditional lender, one in four (24%) have had their application rejected by a bank, a figure that rises to 38% of small businesses that have been in operation for less than five years.

Brokers can help their SME customers find the right finance, and fast.

“Small business lending adds valuable diversity to a broker’s loan book, and we know there are valuable opportunities in this market for brokers,” Reily says.

“It’s important for brokers to realise that there are lending options available where the deal can be closed quickly without taking up considerable chunks of time from a broker or small business owner.”

OnDeck is seeing a lot of “pent-up demand” among consumers that will need to be met, and which small businesses should prepare for by having the teams, inventory and assets in place.

“Now is the time to look ahead, and brokers can provide a value-add service to their small business clients, helping them prepare today for the upswing in demand that history tells us is likely to occur when current restrictions end,” Reily says.

Keeping wheels turning in business

Learning from the shock of 2020, Liberty saw many businesses use the relative stability at the start of this year to put contingencies in place. While many sought finance to expand their operations, others looked to introduce more flexibility within their businesses to provide a greater level of protection against changing circumstances.

Even over the last few months as restrictions were brought back in, businesses used the down time they had as an opportunity to rethink and explore new possibilities, says Liberty’s group sales manager John Mohnacheff.

Recognising the financial challenges that many SMEs were facing, in 2020 Liberty introduced a new dedicated business lending unit to ensure it could provide the support required. As part of the launch of this unit, it introduced two new business lending products, Liberty Access and Liberty Lift – it also remains a participant in the government’s Coronavirus SME Guarantee Scheme and SME Loan Recovery Scheme.

“According to our business partners, our Liberty Lift loan, which provides funds of up to $1m with no mortgage security, has been an ideal solution for many SMEs,” Mohnacheff says.

“For others, financial support is helping to keep the wheels turning through the quieter period. While it’s an undoubtedly difficult time for many businesses, we know from previous experience that a reprieve is coming and that there is a light at the end of the tunnel.”

While supporting SMEs in navigating challenging situations can require brokers to put in a little extra effort, Mohnacheff says it provides a terrific opportunity to build strong, fruitful customer relationships. Liberty offers comprehensive training for mortgage brokers who have not explored SME lending before.

“Providing SME lending support is a fantastic way for mortgage brokers to grow their businesses, as these are among some of the customers in need of the greatest support,” he says.

“Not only can it provide a steady flow of business, but it’s also a great opportunity to use your expertise to help Australian businesses doing it tough.”

As restrictions ease, Liberty expects businesses to need continued support, such as help in arranging loan top-ups or lines of credit while speed picks up, or consolidating any debt they may have accumulated during the lockdown.

Mohnacheff says brokers should stay in close contact with their SME customers as their circumstances can change quickly. He explains that writing an SME loan is only minimally different to writing a mortgage, as long as the information is clear.

“While determining the use of the funds may require some further conversation between the broker and the customer, the application process remains essentially the same,” he says.

“One notable difference is that SME customers often require significantly faster access to funds than a typical mortgage customer. Understanding this, Liberty takes care to deliver fast turnaround times on all SME loan applications to help ensure our business partners can deliver the best customer outcomes.”

Open lines of communication

Although SMEs have certainly felt the effects of the lockdowns, many businesses have rebounded quickly.

In 2020, ING introduced a specific COVID-19 hardship program for SMEs. It saw a big cohort of businesses requesting assistance, but the majority were able to return to normal loan payments within three to six months.

While there are still businesses today that require assistance, the number needing help during the most recent lockdown was much lower than previously, says ING’s national sales manager, commercial, John Kolyvas.

“This time around they are more aware of what’s happening and how it’s impacting them,” he says, adding that ING has also put a bigger focus on understanding the impact on small businesses and how each industry is faring.

ING has also increased its due diligence in order to really understand customers and their needs and make sure they are getting the right level of assistance.

“During the pandemic we have spent time to really understand what small businesses are going through and then passed insights on to brokers so they can be best placed to support their clients.” Kolyvas says.

“Even if they’re just reaching out to their customers to lend an ear, brokers have more experience than SMEs in dealing with banks, and in how banks operate.

“You need to stay proactive. Make sure you’re staying in touch with those customers, even if the customer doesn’t have a need at the moment. Make sure you’re regularly reaching out to them and talking about where they’re at, what they’re doing, and how they’re dealing with the pandemic and dealing with lockdown.”

Kolyvas adds that mortgage brokers who don’t already offer SME lending will probably be surprised at how much they already know.

“Brokers who haven’t done much commercial but deal with a lot of SMEs in processing home loans already understand all of this. It’s just a matter of them being able to articulate it and put it in writing,” he says.

“The other thing I’d say is there can be more reward in lending to SMEs. SMEs have more financing needs; they don’t just have a home loan that they set up and forget for the next four or five years, or buy an investment property and sit on that for however long – SMEs have financing every year.”

Rising confidence in commercial

After the pandemic hit in 2020, commercial property lender Thinktank saw its business customers rearranging their financial affairs to ensure they were prepared if a similar situation were to occur in the future. They established lines of credit and restructured loans to reduce repayments and improve monthly outgoings, freeing up cash flow.

This meant a quieter start to 2021, and while Thinktank has not seen lending for commercial property spike to the levels of residential, commercial property finance solutions are ever-growing, with strong demand in SMSF lending.

There hasn’t been any significant change during the latest round of lockdowns, which reflects borrowers’ greater level of confidence in their ability to withstand current economic challenges.

Thinktank’s general manager, partnerships and distribution, Peter Vala, says there is still positivity in the market, and the lender’s relationship managers are continuing to help SMEs with property purchases, particularly in the SMSF space. Like in residential lending, Thinktank is also seeing a lot of inbound refinance activity, particularly using its mid-doc loans, which do not require financial statements.

“When an SME is seeking finance, their historical financial data may not be the best indicator as to current performance,” Vala says. “This could be due to a period of lower trading, no trading at all, or even as we are often seeing, a spike in trading. Alternative forms of income verification may be more appropriate and fairer to use.”

Vala says now is the perfect time for brokers to speak to their customers, as it’s during difficult times that long-term relationships can be formed.

“Speak to your customers and see how they are tracking. They may be reluctant to ask for assistance, or be unaware of what can be done to assist their cash flow,” Vala says.

“R U OK? Day was a great reminder that it’s important to ask the same thing of your clients: Are they OK? If you don’t, you can be certain many major and second-tier banks will be wanting to edge their way into building new relationships.

“Being there for your clients right now is more important than ever before, to both look after them and your business at the same time.”

Vala also explains that writing a mortgage for commercial property is not significantly different than for a residential property – the same points are covered, just in more depth. For brokers who are unsure of how best to communicate commercial structures and concepts, Thinktank holds free Commercial 101 and 201 workshops.

“Being able to speak the borrower’s language and translate a lender’s requirements makes the broker a valuable resource for any client,” he says.

“Because of this greater level of detail and scope, the loan process with an SME often uncovers more considerations, such as asset replacement needs, working capital or other lending opportunities. It’s one of the reasons why commissions are generally higher in commercial lending, as it reflects the added level of work and ongoing management of the customer’s loan with the lender.”

Ready for SMEs to bounce back

Defining the year as one of “stops and starts”, Prime Capital’s chief commercial officer, Steve Sampson, says the various state lockdowns have meant lending to SMEs has been sporadic. But with the growing vaccine rates and lifting of restrictions over the last couple of months, confidence has been returning.

With 25 years’ experience of supporting SMEs, Sampson says the team at Prime Capital understand the nuances of running a business. Ensuring that SMEs can bridge the gap as they come out of lockdown, Prime Capital has offered support by, for example, reducing interest rates and raising LVRs.

The lender has launched a campaign designed to help businesses get started again. It has reduced its interest rate on its Business Basics Plus loan to 4.95% and increased its LVRs on residential security in capital cities to 75%.

“This will help businesses tap into any equity that they need to, as the prices of property in most states have increased quite a bit,” Sampson says.

“We’re recognising that and giving customers the opportunity to tap into it so that they can make this transition back to normal times as easy and as fast and as simple as possible.”

Prime Capital has also rolled out training webinars for brokers, to support them as they assist SMEs.

The business sectors that will probably need more financial assistance than others include retail, tourism, hospitality and education. But Sampson predicts they will “bounce back with a vengeance”.

“I think we’re going to have a boom market for businesses requiring capital in the coming months as the country returns to normal. And I think that brokers should be really widening their horizons right now,” he says.

“My advice would be to wise up and get the knowledge. Lenders such as Prime Capital have solutions to assist businesses to recover. It’s really fast, and it’s really simple to do. It’s much easier than you might think.

“When you consider that 70% of the Australian workforce are employed by small business, you’ll also be helping many, many people get back on their feet.”

Traditional lines of finance may not be an option for many SMEs, Sampson warns, as they are too cumbersome and difficult. Instead, borrowers will be looking for lenders like Prime Capital that can offer fast, easy finance. This is also where a broker can come in and act as a “solution provider”, looking at the entire breadth of the market.

“Some businesses may need very short finance, and some may need longer as they trade back to normal,” Sampson says.

“These borrowers will remember you for that. When you help them through the tough times, that’s going to give you an opportunity to create tremendous goodwill and long-term relationships with these customers. And at Prime, we really drive to strengthen that relationship between the customer and the broker, and the lender.”