Lenders and brokers discuss state of commercial space

Despite rising inflation, higher interest rates, labour shortages and supply chain issues, commercial lending has held its own over the past 12 months.

Conditions remain strong for many small businesses as they bounce back from the COVID-19 pandemic and look for fast, efficient access to capital.

NAB’s Economic Data Insights EOFY Special Report, covering the week to 2 July 2022, showed a bigger than normal boom in spending almost across the board, combined with very strong business inflows.

“All states except NT and Tasmania gained, with Victoria and NSW,” said NAB Group chief economist Alan Oster. “Results were especially strong in mining, manufacturing, hospitality and construction.”

While the major bank’s monthly business survey for June showed business confidence had fallen to a below-average +1 index point as global uncertainty, interest rate hikes and inflation clouded the outlook, business conditions remained strong across Australia and most industries, including retail.

As the residential property market softens, the opportunity for brokers to boost their business through commercial offerings grows. Supply chain problems mean SMEs need quick access to cash flow.

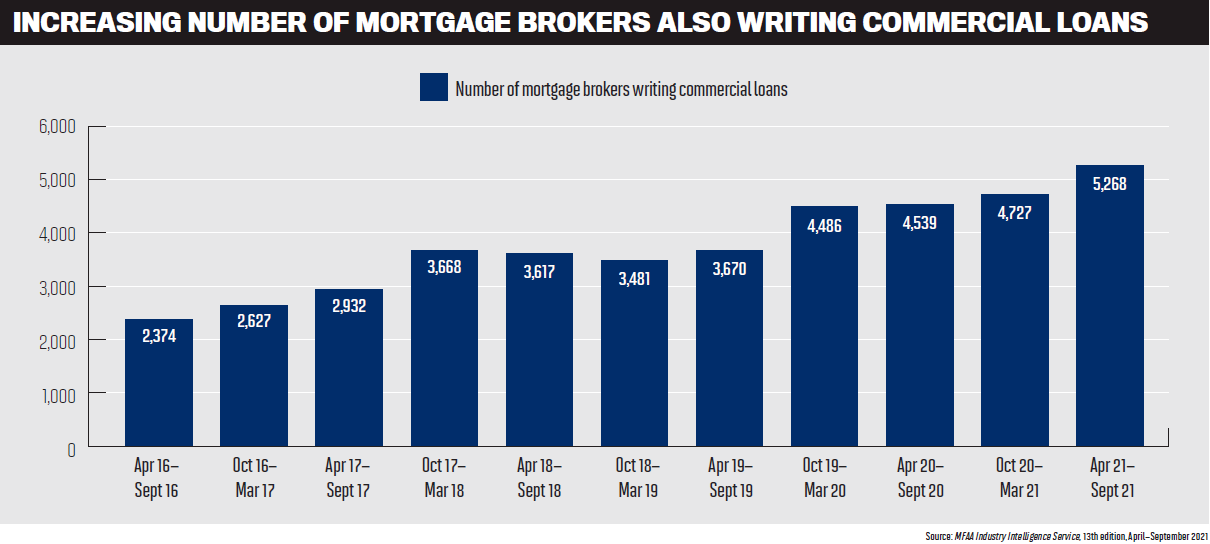

There are also fewer players in commercial broking and therefore less competition. While the latest MFAA Industry Intelligence Service report shows that the number of mortgage brokers also writing commercial loans rose to 5,268 in April–September 2021, this was still just 28.8% of all brokers.

To discuss the opportunities for brokers and the state of the market, MPA brought together some of the major players in commercial finance for its 2022 Commercial Lenders Roundtable, held at Café Sydney.

Attendees included Chris Thomas, executive commercial broker and equipment finance sales, NAB; John Mohnacheff, group sales manager, Liberty; Ivan Mioc, general manager commercial broker, ANZ; Robynne Frost, former executive manager of broker partnerships, business banking, Suncorp Bank; Cory Bannister, senior vice president and chief lending officer, La Trobe Financial; Cameron Poolman, CEO, OnDeck; Jonathan Street, CEO, Thinktank; and Steve Sampson, chief commercial officer, Prime Capital.

Representing commercial brokers were Isabella Constantinou, associate director at Simplicity Loans & Advisory and winner of MPA’s Top Commercial Brokers for 2022, and Nick Wilcox, an associate director at Blue Crane Capital.

Pepper Money head of commercial Malcolm Withers (pictured below) was unable to attend in person but provided his views in writing.

The discussion kicked off with Cory Bannister tackling the first question.

Q: What trends have occurred in the commercial lending space over the last 12 months?

“The last 12 months have been a period of rebound for a lot of the commercial sector post COVID restrictions,” he said. “Some sectors, retail being one, hospitality, tourism – those that you would expect to rebound is what we’ve seen.”

However, Bannister (pictured below) said there were likely to be some headwinds on the way for those sectors, given the Reserve Bank’s two 50 basis point increases to the official cash rate in June and July. He said that while it had been a really strong 12 months of rebound for retail, hospitality and tourism, “they’re not out of the woods yet”.

“Industrial logistics, on the back of the e-commerce boom, has done incredibly well and is likely to prosper for the foreseeable future,” Bannister said.

Office attendance had recovered better than expected, with more and more employers now calling for staff to come back in.

“The final component we see good demand for is construction, which is one area of commercial that’s had a really challenging 12 months, and it’s likely to have another challenging 12 to 24 months in relation to supply issues and staff shortages.”

La Trobe Financial remains calm but cautious regarding construction, Bannister said. “It’s a really finely balanced segment that requires lenders’ support to ensure the sector continues to progress. However, you do need to go about it in a really careful and cautious way.”

He said commercial was a natural hedge against inflation, and it was an asset class that, despite some challenges, was likely to attract further strong demand and perform well over the next few years as “residential cools a little bit”.

“There’s still huge pockets of investor capital chasing high-quality assets which produce a good yield with less volatility than perhaps equities or crypto, for example – both of which were popular in the last two or three years.”

Robynne Frost (pictured below) said that in the small business sector, Suncorp Bank had seen businesses increasingly purchasing their own premises.

“So that’s to escape the fear of being at the mercy of the landlord via increases in rent, and [due to] concerns about landlord hard-ship or selling to capitalise on property values,” she said.

“We’ve also seen a lot more confidence in start-up businesses prepared to take on significant debt, which is encouraging.”

Frost said Suncorp Bank had seen strong demand for property development finance, supported by buyer demand and availability of residential property, but there had been supply challenges impacting the availability and price of building materials.

She has also seen a significant increase in lending for warehousing, due to growth in demand from property developers as well as renovators.

“Developers are now actually either getting all of the supplies up front, storing them, or even asking their suppliers to hold on to them. Quite a few developers have gone under recently because of supply issues,” said Frost.

Chris Thomas (pictured below) concurred, adding that regional Australia was another part of the economy that was growing strongly.

“We have the largest agri bank across Australia, and what we’re seeing is that the global instability is continuing good, strong demand for Australian produce,” he said.

“Despite some of the weather challenges, including floods, regional Australians are really living up to their reputation, and their farmers are very resilient. They are in extremely good shape. They are looking to expand, and their only constraint is essentially lack of labour.”

Thomas said labour shortages were an ongoing concern in capital cities for trading businesses but more acutely in regional parts of the country. “But the positivity of that is it’s forcing innovation, and we’re a seeing strong demand for equipment financing as farmers move to future-proof their busi-nesses through automation.”

The flow-on effect was that for the first time in a long time, resilient country towns were growing beyond their traditional footprint of families and communities, “which is driving more businesses and population growth”, Thomas said.

He said this was exciting because these regional towns have positive infrastructure and great communities but have struggled to attract people in the past.

“Now it’s drawing people to them. Maybe the pandemic has brought a shift back to understanding what the opportunities are in regional Australia,” he said.

Commenting on the SME market, Steve Sampson (pictured below) said small businesses were coming to Prime Capital for funding. “We’re seeing the requirements for working capital for customers that used to be bankable a couple of years ago who are now finding it difficult to get working capital from the majors,” he said. “A lot of customers are coming to us; we’re basically bridging them while they’re recovering so that they can be bankable again.”

Sampson said SMEs also wanted funds quickly. He agreed with Frost’s earlier point about tenancy issues. “With interest rates being low, it’s been cheaper to buy premises than to rent premises. Commercial purchases are at the fore; as the economy picks up, we’ll see more and more of that happening I think.”

Adding to Thomas’s comments about agri finance, Frost said Suncorp Bank had a strong agri book.

“A strong trend we’re seeing is succession planning [in farming]. Mum and dad are moving out or retiring, and the kids are taking over,” she said.

Cameron Poolman (pictured below) said OnDeck, like the other lenders, saw the same trends in terms of commercial finance growth across the board.

“We’re seeing probably a bit more granularity in construction – the ones that we’re wary about are the fixed-price contracts; builders are stuck with supply chain inflationary pressures,” said Poolman.

Australia also differed slightly from other overseas markets, Poolman said. “You look to the US – everyone’s quite pessimistic about how the world’s going to look and around consumer confidence, and we don’t feel like that.

“Matt Comyn [Commonwealth Bank CEO] just came back from the US with a similar perspective that Australia may not be as negatively impacted as what we’re seeing in the US.”

Poolman said small businesses were borrowing money to add cash because the supply chain was really difficult, and they just didn’t have time to access capital when an order came in.

“And so that’s a new thing for us. They actually don’t have a purpose; they just want cash.”

Sampson said SMEs were experiencing a “perfect storm”, in that they were not able to get cash but their property values had increased over the last few years, so they could tap into those properties to secure cash to get them through.

Thomas said this highlighted that brokers, bankers working with brokers, and their credit teams really needed to understand all elements of the supply chain.

“Unpicking that for customers really does present an opportunity for brokers to present lots of different solutions to speed up the access to capital. Access to capital still remains a big issue,” he said.

Due to the lack of staff, the aspiration to “own four restaurants is gone”, Poolman added. “They’re going to own one and have a really cool online offering and invest in that,” he said. “And so utilise things that don’t require people. I’m not sure how that’s going to play out into the future.”

At ANZ, Ivan Mioc (pictured below) said the need for working capital wasn’t a trend a year ago.

“I think the pandemic put a lot of deposits into the banks,” he said. “Now we’re starting to see that probably taper off, and the requirement for working capital has started to pick up.”

Cafes, restaurants and accommodation industries were lifting, he added. “I think local accommodation, particularly in the country, is starting to really pick up; where perhaps pre-pandemic people were probably travelling more overseas, now they’re moving around Australia.”

Malcolm Withers said Pepper Money had seen customers needing help and assistance across three keys areas: debt structuring, access to longer loan terms, and access to higher LVRs.

“This has provided customers with access to debt solutions that empower them, using a loan structure that best works for them, whether it be reduced repayments through longer loan terms, reducing the deposit needed to enter the commercial property market, or debt consolidation allowing the customer to refinance their debts to a lower repayment.”

Q: What sectors of the economy are thriving and need finance? For Liberty the biggest trend was a change in financial planning, said John Mohnacheff.

“The moment financial advisers went fee-for-service, they were less inclined to protect their asset base. More and more of them are starting to say, ‘well, you really do need a diversified portfolio beyond managed funds’. As a result, we’ve seen an enormous spike in self-managed funds and limited recourse borrowing arrangements,” Mohnacheff said.

Agreeing with Bannister’s point about businesses changing from rentals to property purchases, he said business owners were now able to make large lump-sum contributions through their super funds and use that asset to buy a commercial property.

“That’s burgeoning. It’s a really wonderful thing,” Mohnacheff said. “Financial planners are starting to get on board and are recommending that. So the trend is working more closely with financial planners, and that’s an absolute benefit for the entire economy.”

Thinktank had also seen a significant shift in its borrowers, said Jonathan Street (pictured below).

About 90% of Thinktank borrowers are self-employed SMEs, and 80% have been self-employed for five years or more.

“Where these borrowers would have come to us in the past and borrowed through personal names, companies or trusts, they’re increasingly shifting to self-managed super funds because of the long-term wealth advantages of those, plus the ability to manage cash flow effectively,” said Street.

Business owners could also put surplus funds into their SMSFs or adjust rent within the current market range to manage their cash flow in the business.

Street said SMSFs were also an asset protection mechanism: if COVID-19 lock-downs or other unforeseen circumstances arose, the property in the SMSF was protected from other creditors.

A lot of commercial borrowing was attached to warehouse and industrial, he said, with borrowers looking to acquire premises so they could run a “business that will be flexible and adaptable under changing circumstances”, particularly in infrastructure, support services, logistics and distribution.

“It’s the same themes that Steve and Cameron mentioned around cash flow and managing their borrowings to give them extra flexibility should different circum-stances present,” Street said.

“We’re also seeing a lot of professionals moving back out to the suburbs and buying property there because of the decentralisation away from the CBDs and hybrid working.”

Street said it was a great time for brokers because there were more reasons to talk to their clients and support their business referrers with options for lending in multiple ways.

Withers’ view was that industries performing strongly included those that serviced the digital economy, businesses that provided bespoke manufacturing of parts, and the energy industry, which had grown significantly in the past few years.

“This has resulted in strong performance in assets such as warehouse/industrial, and we are seeing a strong appetite by investors for recovering assets such as retail and strata management, especially in suburban areas,” he said.

Isabella Constantinou (pictured below) said everyone was sharing great insights.

She said more was happening in the industrial space in terms of commercial and investment assets, with businesses looking to improve logistics. She also highlighted the growing regional centres as an opportunity for growth for investors and developers.

“One area that I particularly have seen a lot of growth in recently is regional property,” Constantinou said.

Where developers had typically “played in the metro areas”, they were now seeking regional areas to set up land hubs and tap into growing regional markets. “I definitely see that in the property development space as some potential for growth there.”

But Constantinou said the biggest recent trend was clients being uncertain about what they wanted to do. “They might come to us with an inquiry and then take three months to decide whether they actually want to proceed with it, whereas typically, it might have taken three weeks.”

Nick Wilcox (pictured below) said industrial finance was the top priority for his clients.

“Traditionally, my clients have been a mix of SME borrowers and commercial investors. They previously would have wanted to buy a house or a resi investment property, but now they are becoming more educated on the appeal of commercial property, yields and capital growth for certain asset classes. Also, we’ve seen an uplift in PAYG clients also getting into commercial investment properties,” Wilcox said.

“It’s a lot more common now to buy a commercial property; there’s lenders doing lease-doc [loans], doing a lot of them at 70% LVR.

“A lot of lenders also help clients with buying their owner-occupied property at 80% to 85% LVR, with low rates over a 30-year term, similar to a home loan repayment structure which helps with cash flow.”

Wilcox said he had a lot of clients with SMSFs, both for investment and owner-occupier purchases, but mainly commercial.

Q: How are rising costs, higher interest rates, supply chain issues and staff shortages affecting businesses and commercial lending?

Frost said SMEs were operating in different ways to complement or maximise their cash flow. “A trend we’re seeing is more businesses with outstanding tax debt, and the government is now starting to offer formalised, structured repayments. This illustrates businesses have been struggling with cash flow.”

In addition, Suncorp Bank has been seeing a trend of businesses choosing to arrange monthly payments for services such as electricity instead of paying them off on a yearly basis, Frost said.

Sampson pointed out that interest rates hadn’t really kicked in yet. “So it’s hard to say really how business is going, because we’ve never written as much business, but that might be a part of the market that we operate in to help those customers and get from A to B.”

Construction had experienced pain points, including the fallout caused by large building companies getting into trouble due to supply chain problems and interest rates, which were only going to get worse, Sampson said.

“Counterbalancing that, you’ve got businesses that are bringing back manufacturing to Australia because of those reasons, and that has got a direct flow-on then to property.”

Manufacturing businesses were looking for industrial property, and he believed this was a good thing for the economy.

“One thing that’s come out of a pandemic is that we’ve realised that we can’t control the supply chain, and it’s going to run havoc with our economy until we do,” Sampson said.

Poolman said small businesses were impacted by consumer confidence, which had dropped, but this may have been affected by people coming out of the pandemic.

“Traditionally, we look at discretionary spending and see what small businesses are impacted by that, but we just haven’t seen them impacted yet, so that’s something we’re watching really carefully.”

Short-term unsecured loans offered by OnDeck were not generally promoted through advisers, Poolman said. “We’re speaking to a lot of our customers – their accountants are actually saying this is a good idea for you to have this cash available to do what you want with.”

Bannister said labour was also causing an issue. “We really need to accelerate migration back to those historically normalised levels. Everywhere you look there’s labour shortages.”

He said the shortage of workers was creating pressure, both in terms of having people actually doing the work, but also its impact on wages: in some sectors, wages had been pushed to record levels.

“In our sector, for instance, the cost of recruitment has increased significantly, and I query the sustainability of that shift.”

This was “super important” to solve a lot of challenges for commercial and SME businesses, Bannister said.

Mohnacheff (pictured below) said immigration was the key to addressing staff shortages. He said if Australia adopted the new policy (which had been in place in New Zealand for years), which he described as a “wonderful, welcoming approach to labour”, it would go a “long, long way to fixing our supply chain issues and our labour shortages”.

“They’re not going to come in and start farming in the major cities,” Mohnacheff said. “They will come and actively work in these emerging wonderful rural communities which have been horribly underserviced.”

Thomas switched the discussion to interest rates, which he said were very topical.

“We’re still in a very low interest rate environment, particularly around the commercial side,” he said. “This is a fantastic opportunity for commercial brokers to be able to unpack for their clients what a rising interest rate environment looks like and put context around it, in respect to what the opportunity is of investing in their business.”

Thomas said if the trusted adviser emerged from that, it would be someone offering advice and comfort by dissecting the impact of rates and other challenges affecting SMEs.

“Interest rates rising alone should not be a deterrent from future business investment when this country has such a fantastic opportunity to seize the day,” he said.

Thomas agreed with Poolman’s comment about Australia being in a good position. “We have to keep reminding ourselves of that sometimes, and not getting caught in the headline,” he said.

Street echoed Thomas’s comments and said low interest rates and intense competition meant that the cost of borrowing had insulated businesses’ ability to contend with these factors.

“As rates rise, there will be an increasing challenge for borrowers and businesses to deal with these very front and centre issues that aren’t going away any time soon,” he said.

“It’s the best time for brokers to be closely involved with their clients to help them through the many challenges that we’re going to have ahead, because cash flow is going to tighten quite a lot over the coming months.”

Mohnacheff added that the ATO had returned to its pre-COVID debt collection diligence. “They were on a little hiatus for two years as many struggled through COVID lockdowns and hardship, but the government collection agency is now going to be quite serious in collecting that [tax debt].

“Brokers should be aware, not panic. There are lenders out there who don’t mind tax debt. Right? You’ve got a tax debt because you’ve made a profit.”

Mioc said ANZ knew that businesses were resilient. “The pandemic has taught us that. They’ve adapted to new ways of operating, and I think most points about labour are right, and all the things we’ve spoken to.

“But I genuinely think that we’ve got a strong economy backed well by financiers, and I think businesses will see this through; we’ve already seen that.”

In response, Street said: “Well, the last thing the RBA wants to do is pull the rug out. They don’t want to see unemployment dramatically rise; they don’t want to precipitate widespread business failures.”

Q: There’s a record number of mortgage brokers moving into commercial finance. What’s attracting them?

Wilcox said for most brokers the attraction to commercial was to be able to help their clients with all their finance needs, ensuring they were offering the full suite of lending options for property transactions. If the residential broker referred their client to a commercial broker, they could be at risk of losing the client altogether, so those trusted partnerships were important, he said.

“It’s hard to say no to a client. Most mort-gage brokers are individual operators, so if you’ve got a network of clients and you get an opportunity, it’s a difficult conversation to turn a client away or on to another operator.”

It was also getting easier for brokers to offer commercial lending in the investment and owner-occupier spaces, Wilcox said, adding that trade publications such as MPA were also encouraging brokers to diversify.

However, “there’s some brokers that don’t want to do it,” he said. “I get residential brokers giving us deals who say, ‘I want to stick in my lane; I’ll give you the commercial’.”

Constantinou agreed that there were definitely opportunities for residential brokers to diversify into commercial.

“Since COVID, there’s been such immense competition in the market with some of the major banks that pulled out of certain assets in commercial lending,” she said. “There was so much competition in the non-bank space and so much opportunity for alternative lending solutions.

“Like Nick said, the lease-doc solution is a very easy way for resi brokers to write some commercial business if they see that their client has an investment property in their portfolio. It’s a very simple way to start.”

Constantinou said residential brokers could easily dabble in commercial finance if they had a fundamental base knowledge of it.

“I think there’s a great support system within the industry to help resi brokers gain more knowledge on how to play in the commercial space.”

Residential brokers could get involved in commercial lending through a referral network or by writing business directly through banks, she pointed out.

“If you’re trying to do both, say, 50–50, that’s where it becomes quite difficult, because the home loan space is so regulated; there’s so many policies that don’t necessarily apply to commercial,” said Constantinou.

Mioc said the broker aggregators had done a really good job of promoting diversification through their education streams.

“That’s great from the aggregators’ perspective but also for the brokers to be offering a full service to their clients, and as Nick mentioned, the additional income stream is also valuable for brokers,” he said.

“We invest heavily in making sure that as brokers are diversifying, they’re getting the right education; they’re learning about the complexity of servicing commercial customers. So, I think, more broadly, the industry is kind of pushing this way, which allows the broker to retain and then grow stronger relationships with their customers, and I think that’s an absolute trend in the industry.”

Sampson said the home loan market was very crowded, so he questioned whether brokers would want to play in that pool or would find it easier going elsewhere.

“My BDMs this year are not BDMs in the real sense; they’re coaches and they’re trainers. We’re spending a lot of time talking to brokers about how we operate, our differences, and how easy it can be to write commercial finance.”

Sampson said every time Prime Capital did a webinar or training “we’ll get an application that brokers didn’t know they could set, and very soon after we get another one”.

It was up to commercial SME lenders in the space to educate brokers, he said.

“I think the stat is 28% of [residential] brokers have written one commercial loan last year. It should be a lot more than that. They’ve got self-employed people on their books. We try and teach our brokers how to mine that database to see who might be avail-able and how we can really make them solution providers as against just brokers.”

Diversification had been a long time in the making, said Street, who praised the good work of aggregators, industry associations such as the MFAA and FBAA, and lenders for educating brokers and helping them work shop deals so their clients could take advantage of lending opportunities.

“What we’re seeing more recently is just the broader lender landscape has become much more broker friendly. The majors used to try and resist dealing with brokers and commercial, but now they’ve had a renaissance and they’re actively out there supporting and offering better deals, better engagement, better processes.”

Street said there was still a long way to go, but it “was coming together with a lot of effort across the industry”.

Another emerging trend, said Frost, was an increase in people choosing broking as a career. “We’re seeing a lot more commercial bankers [shift into broking], and it’s a credit to all of us in the room that have been involved in the industry.”

Frost said broking was not only an incredible career choice but would lead to growth in commercial finance.

“I think that by having more experienced commercial bankers join the industry, this has really helped us balance out the skill base of brokers.

“There’s a big difference between a lazy commercial transaction crossing a home loan broker’s desk, as opposed to a good-quality broker who is really committed to diversification.”

Frost said there were plenty of options for brokers; “if it’s just the one [commercial] transaction, a referral program is a better outcome for that customer”.

Mioc agreed there had been a trend of new brokers being accredited who were formerly commercial and corporate bankers and “really understand the complexity of commercial transactions”, and perhaps that wasn’t happening pre-pandemic.

“We’ve seen more mortgage brokers diversify, and we’re seeing more good commercial and corporate bankers entering the commercial broker industry,” Mioc said.

Thomas supported the point that growth was coming from both mortgage brokers moving into commercial and the ex-business banker who wanted to become a commercial broker.

“Touching on the industry bodies and the aggregators, I would say the work has only just begun,” he said, “because a number of the bankers going into broking get quickly consumed by volume and need to spend time on their businesses.”

He said there was a great opportunity for the industry to support new small business owners in growing their businesses over and above customer interactions and transactions by helping them recruit staff, develop their strategies and build their businesses.

He added that mortgage brokers also had to ask themselves: What was their core? What was their value proposition? How did it fit into a broader strategy? “Commercial may not be for everyone, just as mortgages are not just for everyone,” Thomas said.

Sampson argued that the more diversified a broker’s book was, the more valuable it was – that had been proven many times. “So, if they have a mix of home loans, commercial and leasing, you’re going have a much more valuable business.”

Street said it was also a defensive play for brokers to offer that wider value proposition. “So, if the client is going to think about their need for residential, commercial, or other types of finance, they ring their broker first and not the bank, or may be introduced to another broker via an accountant or a lawyer. So they become more of a relationship manager and control the client link.”

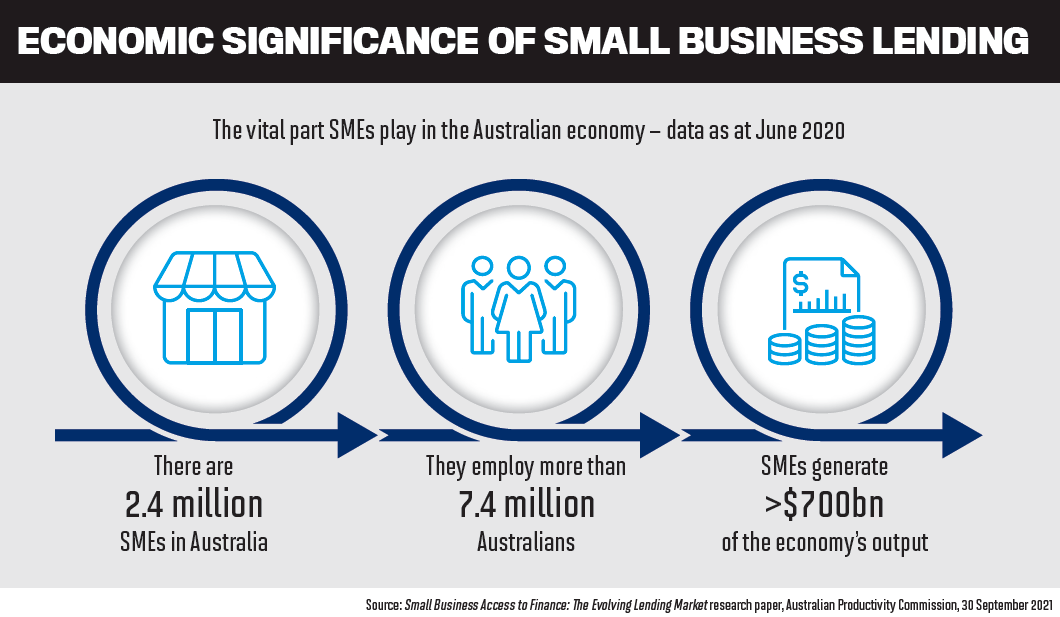

Poolman agreed. He said that with 2.4 million small businesses in Australia and one in five consumers running a small business, there were big opportunities for brokers.

“When I first started, only 50% of people used a mortgage broker; now it’s 70% – so these guys are actually going to use a broker to get their commercial finance.

“If you don’t do it, they’re going to go somewhere else. Do you want to hand your relationship to someone else? Everyone’s getting better at engaging with brokers from a funding point of view.

“In our type of product, it’s six months of bank statements and you’ve got an approval in two hours, and that’s actually getting easier for the brokers to deal with and service the customer.”

Withers said that despite supply chain disruptions, increasing expenses, staff short-ages and wage pressure, SMEs were confident about pivoting their businesses and finding new opportunities to thrive.

“Many SME owners are looking to invest more into their businesses post-pandemic. The opportunities for brokers are there, especially with an estimated two million SMEs in Australia desiring a trusted busi-ness adviser. Brokers are increasingly sought after to help SMEs achieve their short- and long-term business goals.”

Q: What are the advantages for brokers diversifying into commercial lending, and how do you support them to be successful?

Constantinou said the commercial space was so complex and vast compared to resi-dential finance. “I think what deters a lot of residential brokers is that there’s so many different facets of it. Maybe they don’t know where to start.”

From an educational and professional development perspective, Constantinou said there was a long growth trajectory for a residential broker’s business.

“They can pick one segment, learn what they need to learn, start playing in that area of commercial, and then once they’ve got their handle on that, move into something else and slowly grow their business until such point where they might be writing a little bit in all segments of the commercial lending space.”

Having a support network and being educated by industry bodies and lenders was key so brokers didn’t feel commercial lending was “a daunting space to enter into”, she said.

Read more: Women can shine in finance industry.

Wilcox said the aggregators, the MFAA and banks were now doing a much better job of supporting brokers to diversify into commercial finance. Formerly a small business banker at St. George Bank for six years, he said a lot of residential brokers would contact him, and he would educate them or write a deal for them.

Mohnacheff said a very interesting statistic illustrated the importance of commercial lending.

“If you ask any family that’s taken a home loan through a broker and in two years’ time ask them who the broker was, 95% will not be able to tell you – fact,” he said.

“It’s been proven by Aussie and all the big resi writers: it’s very difficult just to remember that one transaction. But when you have a commercial transaction with a broker, you don’t do it like, ‘oh, I’ve got to get rid of this customer really quick; I only want to touch them once, I want to move on to my next deal’ – you work with that individual.”

The connections or “sinews” between a commercial customer and their broker were far stronger, said Mohnacheff. “Commercial people will go back to the well again and again. Once they’re there, it’s wonderful repeat business, and as their business grows, so will the broker’s business. There’s so many more touchpoints along the life cycle of a commercial loan than there ever is in a home loan.”

Bannister said there were four key benefits to broker diversification.

Firstly, it would diversify the broker’s revenue stream. “You haven’t got all your eggs in a particular segment of the market, so if you’re a residential broker and the market turns, you’re not left exposed,” he said. “I think it’s really important when we talked about the rising-rate environment, commercial being a natural hedge.”

The second benefit for brokers was being able to market themselves to a wider audience and originate more customers who supported the broker’s residential business.

Thirdly, the broker could protect their revenue stream by protecting their customer footprint. “Because if you don’t service them, they will call the bank or another broker, and once they’re gone for the commercial transaction, as to John’s point, you helped them during the hardest stuff; the easy stuff goes as well.”

Bannister said the fourth benefit was protection against regulatory change. “Up until two months ago, we still had the spectre of a rem [remuneration] review hanging over the broker industry. Thankfully, that appears to have been stayed for now, but one thing 2020 taught us is to expect the unexpected, and don’t think that perhaps it won’t go around again. So I think commercial could be looked at as regulatory hedge to the residential space.”

Frost said one area where more support could be required was with the lending choices commercial brokers offered to clients.

“We talk about best interest duty – more commercial brokers are talking to us about ‘we want to make sure we’re providing the right choice for our customers’,” she said.

“I actually think, as a collective industry, we have to do a better job of keeping our brokers informed of all commercial product choices available to their customers.”

Frost admitted it would require extensive lender support, but she said it definitely warranted consideration.

From a broker’s perspective, Constantinou said it was an “out of sight, out of mind thing”.

“We deal with the lenders that we speak to and see and have something to do with regularly. The other ones just get lost in that noise of blasts from the BDMs about new policies or rates,” she said.

“Some lenders would see more business just by appearing in front of us and saying, ‘Hey, guys, this is our offering. This is how we can support you as brokers; this is how we can support your clients; and this is where we have a distinguishing factor for a lot of transactions’. ”

Constantinou said this was a key factor, and she tended to use the same lenders over and over again because it was self-fulfilling.

“I end up building a better relationship with those certain BDMs, so then we’re able to facilitate what we think is a better option for the client, but there might be something out there that we’re not even aware of, because some of the banks just may not be as forefront for us,” she said.

Withers said momentum was continuing to build for brokers eager to diversify into commercial lending.

“Brokers can diversify their revenue stream and build stronger relationships with clients not just for home loans but for those looking for business solutions also,” he said.

He said Pepper Money tools such as the Pepper Product Selector, over 20 years of specialist and SME knowledge, dedicated BDMs around Australia, and a real-life approach to making deals happen created a game changer for business owners and brokers.

“We are long-term advocates for the training and education of brokers, and actively support brokers with regular training,” Withers said.

“Our current training program covers technical-based training on our products and policies, assessing customers’ income and servicing, as well as training focused on developing confidence by giving brokers the tools they need to identify an opportunity and have a quality conversation around it.”

Sampson said one of the approaches Prime Capital took was to not just teach or show brokers the products but actually show them the market. “So, where is the commercial market, the SME market? Where are the gaps in that market? How can you fulfil them? And how can you actually mine your database to find those little pearls that will diversify your business?”

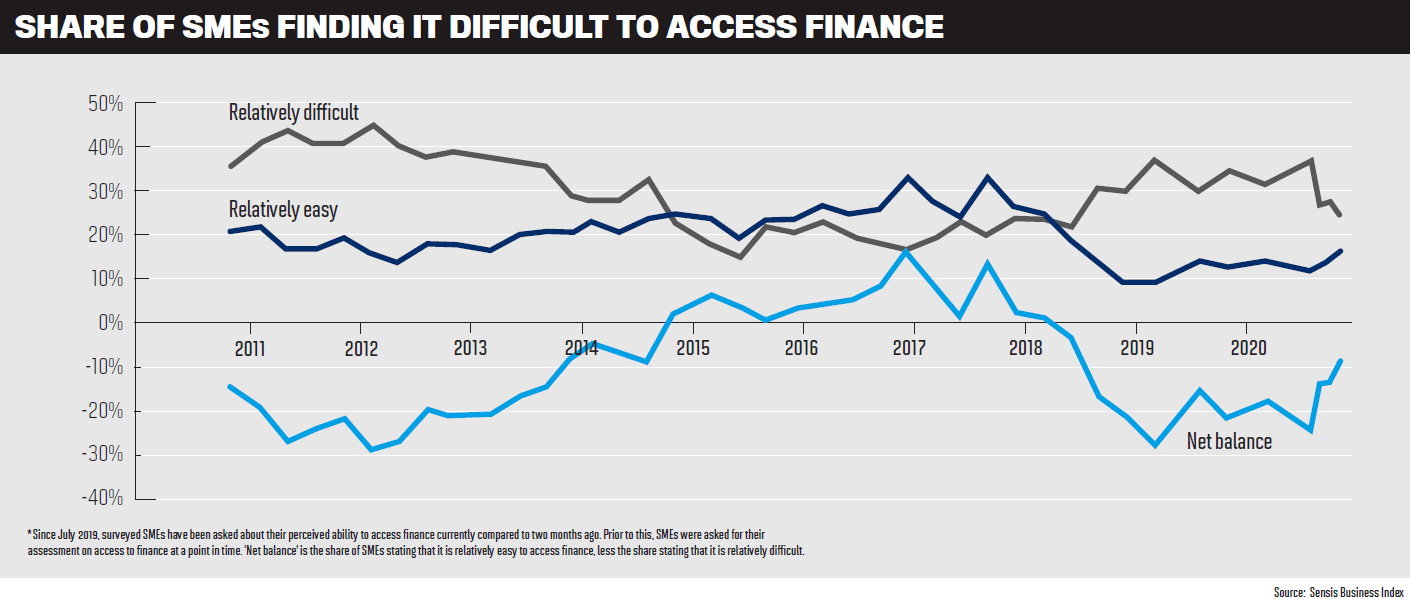

Q: Some studies have shown that SMEs find it difficult to access finance, or don’t know where to go. How are you reaching these customers and ensuring a smooth loan process for brokers and clients?

Thomas said the question about access to capital was one that came up regularly. “So clearly, as an industry, we have to keep working harder at connecting to the 2.4 million small businesses, and for NAB’s part, what we promise to brokers is that we will give you access to the best of NAB.

“With many agricentres, business centres in metropolitan areas, a lot of specialists and support bankers, our BDMs, all up on any one given day we’ll have about 800 of our colleagues connecting with brokers. We want to support those brokers to connect with more customers.”

Regional locations were as important as metro locations in making sure all clients that needed support had those connectivity points, Thomas said. “Part of it’s about products and services, but a lot of it’s about insight and partnership. We very clearly see brokers as trusted advisers.”

Thomas said the role NAB looked to play with its brokers was to give them access to what it had as a big national bank and allow them to draw down on those products, services, insights and advice to support them in their conversations.

He said the bank wanted to build long-term relationships with both brokers and their customers. “That is the essence of commercial relationship banking, relation-ship broking: be there three, four times a year for them when they need you.”

Thinktank deals only with brokers, so Street said the non-bank’s job was to support brokers and their clients.

He said whether brokers were seeking alternative verification loans that were faster and simpler, or an equity release, an 80% LVR, or a loan size of up to $4m, Thinktank wanted them to have a succinct view of what it could offer as a lender and where it wasn’t able to help.

“It’s all about being clear with brokers as to where we can help, so we don’t waste their time,” Street said. “It’s really just making sure that our business sits behind the broker, helping them build their business. We’re not after access to the client or the client relationship. It’s about making sure that the broker has all the support, tools and information that helps them do their job as quickly and as efficiently as they can.”

Mohnacheff said Liberty was also purely broker, and one of the niches it had relied on for a very long time was accountants.

“Brokers would say to us, ‘we’re struggling getting referral sources’, and we would say, ‘have you tried accountants?’

“You go to an accountant because you’re the one to start a company, to help companies in financial difficulty, or to assist those with an ATO debt, right? That’s small businesses; that’s why they go to an accountant. They don’t go to an accountant and say, ‘can you give me a home loan?’ ”

But Mohnacheff said that if brokers went to an accountant and said, “Do you have any customers that have an ATO debt, cash flow problems, want to buy a commercial property, or are setting up an SMSF?”, they probably would.

“It is a lay down misère – that’s where they deal.”

Mohnacheff said Liberty helped brokers expand their referral networks by gaining a better understanding of and forming deeper relationships with their accountants.

“There’s thousands; every small business should have or probably does have an accountant. So, forming that bond, and that broker becoming that important link between accountant, borrower and broker is another sinew that we can really help them with. Helping them to diversify by creating deeper and more meaningful referral relationships.”

Wilcox agreed about the value of accountants to a broker’s business.

“I’ve been a broker 12 months, but I was in business banking for six years. All my business previously came from brokers, and they all had accountants. So going out as a broker, I’ll speak to accountants, and they would say, ‘I already have a broker and they’re residential’.

So, Wilcox pivoted by offering commercial finance, taxes, anything non-residential. “My trick is I speak to that accountant, I build a relationship, I go to meet them for coffee.”

Poolman said small businesses would find it easier to access capital if they knew where to look.

“Around this table, we’re all quite complementary to each other in terms of products and customers that we service. If a customer looks directly on to the web or Google, they’re just going to get a result that’s optimised by the funder to service them, where that may not be the right result.”

That business would then say they found it hard to access capital, Poolman said.

“The opportunity as the broker is to present whether it’s equipment, finance, data finance, unsecured finance, property secured, what-ever the right product is for them … I don’t think it’s as hard to access capital as what some people say, if the broker is able to provide them with the right product.”

Bannister said there was more inclusive approach from lenders now. “It’s the breadth and depth of lenders and their solutions I think makes a difference.

“If I go back five or six years ago, it was a pretty steep barrier to entry for a lot of brokers to get into commercial; you had to arrange all of your individual accreditations first. But through the innovation of lenders and their products and the removal of lots of those barriers and just the general accept-ance that we’re willing to help and support brokers who want to have a go, I think has enabled more and more to get involved.”

Sampson said 70% of home loans were handled by mortgage brokers, but the percentage of commercial loans that brokers dealt with was quite low.

“There’s a yawning gap there – a lot of that 70% are going to be small business people. I think it’s a matter of time before those customers that naturally would go to a broker for a home loan should be naturally going to a broker for a commercial loan. The only thing that would stop that is probably that the broker is not offering that.”

Frost sees a huge opportunity in this space. “We’re reaching those customers through our brokers, and we expect more small businesses will be reaching out to brokers to learn how to access finance in the future,” she said. “This is aligned to what we’ve seen in the home lending space, where the majority of home loans are handled by brokers.

“We ensure a smooth loan process for brokers and clients through our specialised business development managers, who have deep industry expertise and are passionate about educating brokers so they can best serve their customers.”

Withers said Pepper Money knows that all businesses are unique, and so are their lending needs. “That’s why we’ve got a range of prime and near prime commercial property loans, including full-doc and alt-doc options for customers who need commercial lending solutions up to $3m in loan size.”

He said the advantages of Pepper Money’s commercial loans included the ability to deliver a fast commitment and provide confidence in lodging a deal.

“We deliver fast assessment that provides a broker direct-to-credit engagement and a fast time to cash where we are able to provide a seamless settlement,” Withers said. “But the biggest thing is allowing the brokers to talk directly to our credit managers, which is really important to ensure the broker is able to tell that customer’s story directly to the credit manager if there are any questions. We stand by the broker every step of the way.”